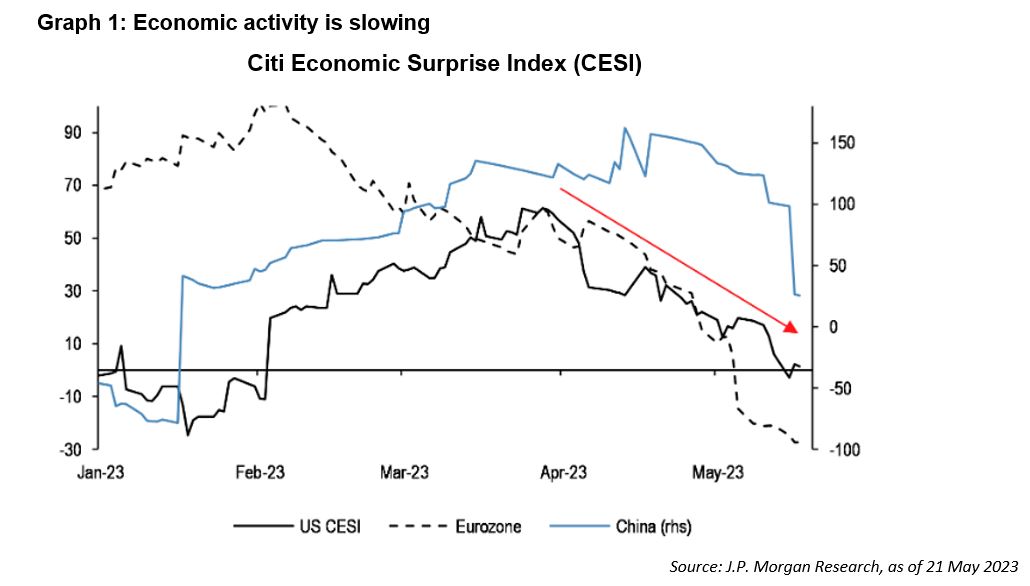

We believe the Fed would err on the side of caution, preferring to maintain rates at this level instead of continuously hiking rates in order to achieve a soft landing. The key risks is if we see a wage spiral effect resulting in a much stickier or even a resurgence in inflation.

That being said, looking at the medium-term, our base-case is that of a gradual global slowdown as monetary policy filters through the real economy. We anticipate an increase in the unemployment rate coupled with the absence of a wage spiral. Consequently, this should lead to a gradual decline in inflationary pressures.

Mild Recession, But Caution Needed…

The case for a hard-landing recession appears to have been dwindled as the US economy maintains its resilience. Excess savings and unleashed demand post-pandemic helped to fuel the services sector, bolstering US gross domestic product (GDP). The labor market remained robust with the unemployment rate holding steady at 3.70%.

However, there are important signposts that bear watching. Companies are already trimming capital expenditure and work hours, with a slight increase in the unemployment rate. Additionally, regional banks are still facing pressure from deposit outflows.

Similarly, we are closely monitoring the commercial real estate loan sector as default rates are on the rise. Granted, these concerns are mitigated by a robust US housing market, characterised by low inventories and relatively low leverage in both the household and corporate sectors.

In the mid to long-term, we believe that the strength the US economy would start to dwindle and experience a gradual deceleration in the coming months, but a hard landing recession is not within our base-case. Instead, we anticipate a mild recession as the impact of tighter monetary policy begins to bite.

However, it is crucial to acknowledge the presence of various downside risks that could change our view on how deep or shallow this recession could go.

China Still Worth a Look

Softer economic growth data has weighed on sentiment of China equities this year. However, attractive valuations do present attractive entry points to add exposure.

Valuations have experienced a notable decline over the past two years as reflected in the MSCI China index which currently trades at a price-to-earnings (P/E) ratio of 10.00x, below its 10-year historical average of 11.30x. Considering a potential normalization of the P/E ratio, we anticipate a favourable upside potential of around 13.00%.

While many other countries have been engaged in interest rate hikes, China has done the opposite by implementing rate cuts. This should filter through the economy and help spur a rebound. In the past month, there has been a growing recognition from Beijing that economic momentum has dwindled. This has prompted a shift in policy tone from Beijing on the need for more concerted stimulus measures.

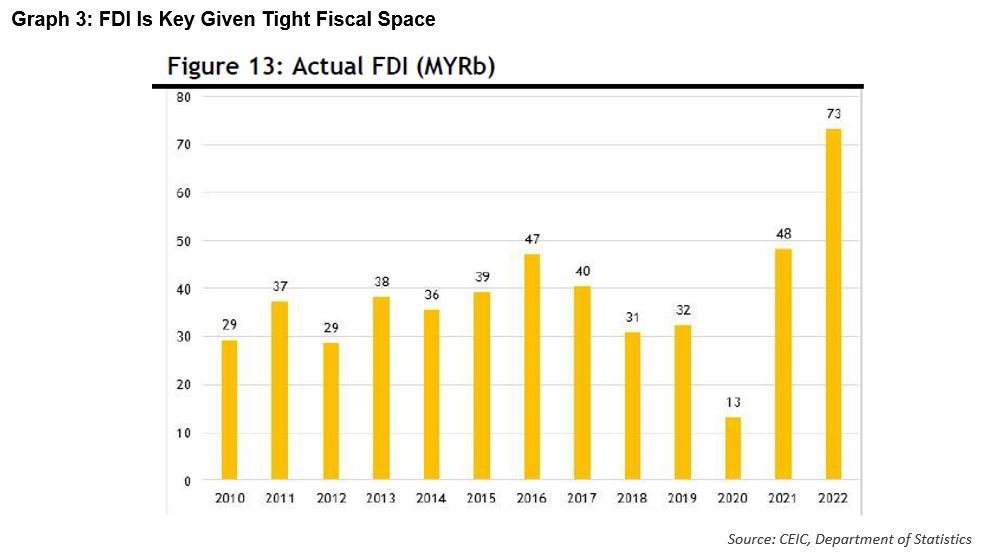

Malaysia Awaiting Clarity

Foreign funds have exerted significant selling pressure on the Malaysian market this year, resulting in lacklustre performance. The market has faced challenges due to a weaker Ringgit and political uncertainty, which have hindered any substantial breakthroughs.

However, we anticipate a turnaround in the 2H’2023 following the conclusion of state elections, which will provide greater clarity on the stability of the unity government.

With a stable government and accommodative policies in place, we anticipate an increase in foreign direct investments (FDI), which will boost market sentiment and provide support to the Ringgit. Notwithstanding macro noises, the domestic economy continues to display resilience, as evidenced by its solid GDP showing.

Current valuations are also favourable with the KLCI being among the most attractively priced in the region and historically on a P/E basis. Once there is greater political clarity, we expect foreign outflows to reverse providing support to markets. Additionally, as the Fed nears the end of its rate hike cycle, there will be reduced pressure on the movement of the Ringgit.

However, it would be also important to see continuous reform measures to instil strong governance and fiscal discipline. The ongoing subsidy rationalisation is crucial in enlarging our fiscal buffers and narrowing our deficit. Alongside public expenditure, the government should continue to prioritise business-friendly policies to incentivise private sector investments which is an area that has shown progress under the new government.

Collectively, these measures will contribute to a stronger economy and a recovery in corporate earnings that serves as key catalysts for the local market.

On portfolio positioning, the bulk of our position is in quality large caps and these names are the prime beneficiaries when foreign flows return to Malaysia. Besides that, we favour healthcare sector which should see strong earnings growth driven by elective surgeries and medical tourism.

Bullish on Bonds

Bond investors would be sufficiently compensated from the yield carry, considering the upward adjustment in bond yields witnessed over the last 2 years. Investment Grade (IG) bonds, on average, offer yields ranging from 5% to 6% in USD, while yields hover around 4% to 4.5% in MYR terms. Furthermore, bonds have historically demonstrated resilience and tend to outperform in a decelerating growth environment.

As the Fed approaches the tail-end of its tightening cycle, we anticipate a potential stabilisation of bond market volatility. This would bolster the defensive attributes of fixed income as a valuable hedge against equity.

In our base-case scenario of a mild recession, we anticipate a continued rise in default rates. Consequently, our preference lies with Investment Grade (IG) bonds rather than High Yield (HY). Within the IG space, we favour sectors that have shown resilience during economic slowdowns and are less susceptible to geopolitical shocks.

We are wary of credits that are highly leveraged credits, as they face elevated risks associated with refinancing and repayment. We remain vigilant of such risks and prefer credits with more favourable risk profiles for our bond portfolios.