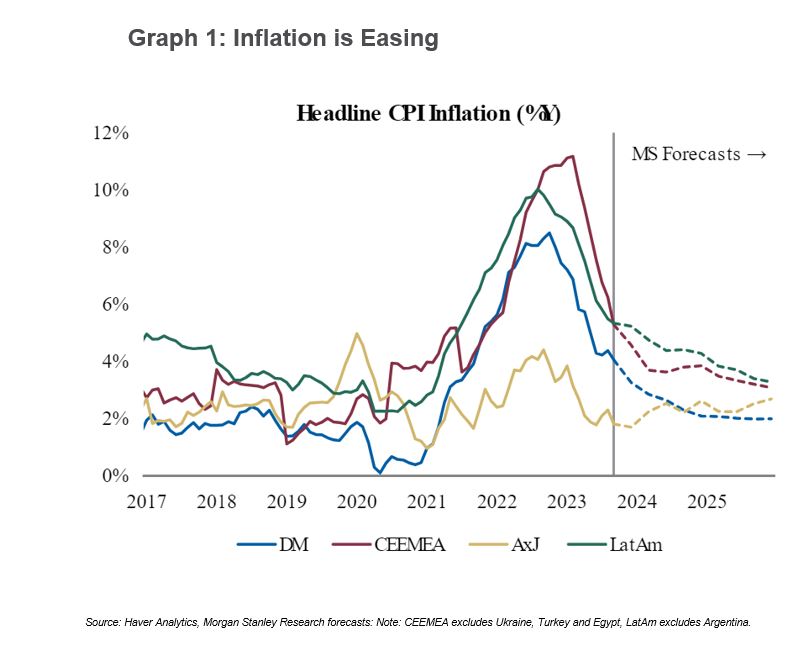

Policy Pivot Brings Tailwinds to Asia

With the focal point of markets shifting away from rate hikes to a rate pause, we see conditions turning more conducive for equities through a more stable interest rate outlook.

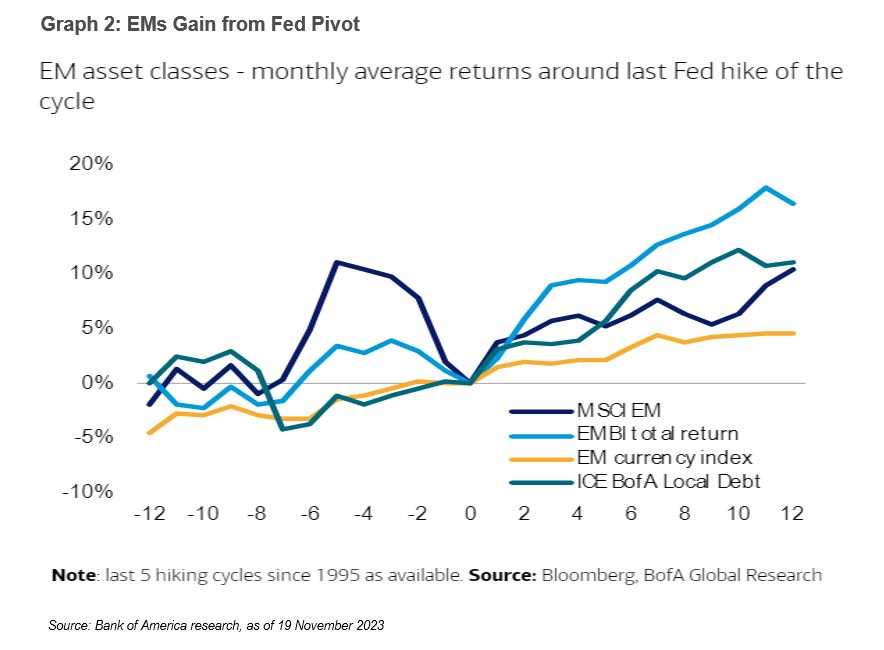

Historical patterns show that markets have generally shown positive performance in the periods after the last Fed hike.Emerging markets (EMs) & Asia are in prime position to benefit as the Fed’s dovish pivot begins to take flight.

In the past five hiking cycles since 1995, EMs have displayed strong outperformance benefitting from an influx of foreign flows and a waning US dollar strength.

Within Asia, Korea and Taiwan are expected to spearhead gains through higher earnings growth.

Almost 40% of Asia's projected earnings growth for 2024-2025 are anticipated to come from Korea and Taiwan tech companies as the sector heads for a cyclical upturn.

The street is currently forecasting an EPS growth of 68.70% for MSCI Korea and 18.20% for the MSCI Taiwan index.

Companies with exposure to artificial intelligence (AI) are standout performers that are expected to deliver strong earnings, propelled by a sustained demand for chips as AI technology continues to mature.

We are also positive on India and Indonesia for their longer-term growth potential within EMs. Positive demographic trends such as rising urbanisation and higher income levels represent structural drivers that would help underpin growth over the years to come.

China Remains a Wildcard

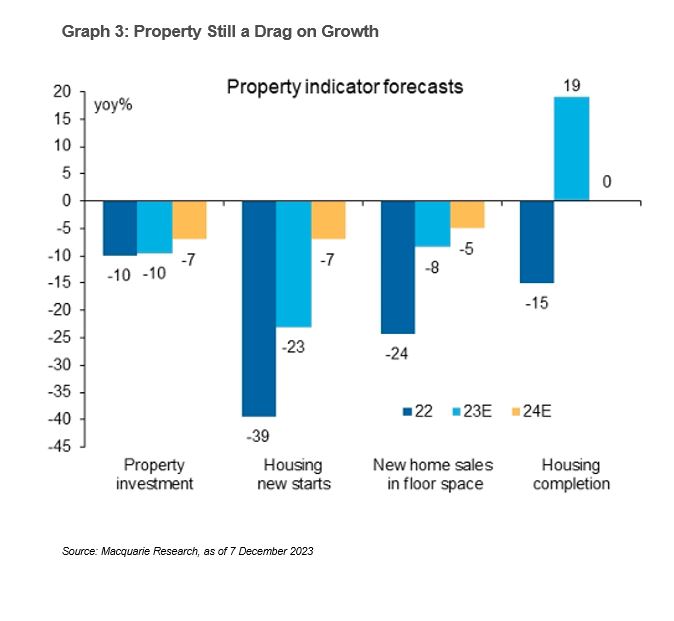

While valuations in China are hovering at multi-year lows, there is still a need for caution as its recovery remains patchy.

A deep rout in its property sector continues to be a drag on growth with new home prices in China declining for the fifth consecutive month in November, according to data from the National Bureau of Statistics (NBS). Similarly, property investments fell 9.40% y-o-y reflecting ongoing challenges in the sector which is strategically important.

Other economic data also points to an uneven recovery across sectors. Industrial output grew 6.60% in November from a year earlier outpacing expectation. However, retail sales missed estimates as analysts had expected a more robust recovery following a low base in 2022 when the economy was hampered by COVID lockdowns.

This sluggish recovery would maintain the call for additional stimulus measures in 2024. Over the past year, Beijing has announced a flurry of policy measures aimed at supporting the beleaguered property sector. These include measures such as providing unsecured loans to eligible developers and issuing 1 trillion renminbi of bonds.

While these steps may provide short-term relief in terms of liquidity, they may not be effective in addressing the fundamental issue of demand.

We are taking a wait-and-see approach for China until there is further clarity on bolder policy actions to arrest the decline in the property sector. Top leaders said they would step up policy adjustments to support economic recovery in 2024, with a focus on boosting domestic demand.

At its annual Central Economic Work Conference held in December, the policy language further stressed on its adherence to proactive fiscal policies as well as prudent monetary policies to navigate the economic landscape.

Carrying On with Bonds

With growing expectations that the Fed has hit peak interest rates, we have increasingly turned more constructive on fixed income, particularly on the carry component. Given the substantial rise in yields over the past 2 years, there is opportunity for investors to lock-in yields with certainty on high-quality bonds.

In past economic cycles which was marked by negative interest rate policies (NIRP) or near-zero interest rates, bond investors often had to venture into higher-risk assets like high-yield (HY) or private credits to boost portfolio yield. However, the current environment presents ample opportunities for investors to extract yield without sacrificing quality.

By investing in global investment-grade (IG) bonds, investors can generate a decent carry in the range of 5%-6% without assuming excessive credit risk.

Furthermore, as we draw closer to a rate cut cycle in 2024, investors stand to benefit from potential capital gains. Even if inflation occurs at a slower pace than expected and interest rates stay higher-for-longer, bond investors are still compensated through the positive carry.

Our preference lies with investment-grade (IG) over high-yield (HY) in this current environment. At current levels, investors don’t have to take on too much credit risk, while still getting decent portfolio yield.

Malaysia Outlook | Moderating Growth & Inflation

Locally, Malaysia’s full-year GDP growth is expected to average around 4.0% in 2023 supported by strong private consumption. However, economic momentum may start to dwindle in 2024 as we witness a recalibration in spending patterns among consumers due to subsidy rationalisation.

An increase in the sales and services tax (SST) rate to 8% could exert further pressure on spending as consumers refrain from high-value purchases.

In terms of inflation, near-term expectations are subdued. While there are upside risks to inflation due to necessary subsidy rationalisation measures, they are unlikely to prompt any policy adjustments by Bank Negara Malaysia (BNM) on the overnight policy rate (OPR).

Bond markets have currently priced-in the peak of terminal rates at 3.00%, assuming the absence of any inflationary shocks.

Fixed Income | Technicals are Favourable

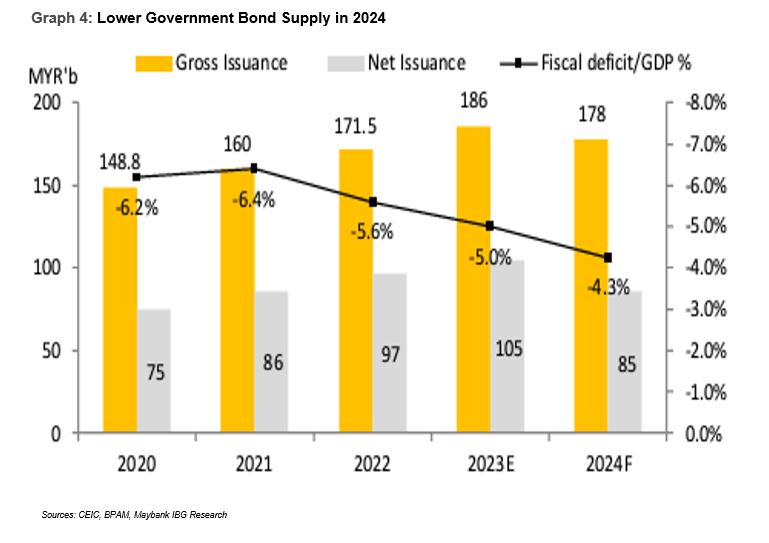

As the government continues along its fiscal consolidation path, we expect a lower government bond supply next year.

The government is targeting a fiscal deficit of 4.30% in 2024 which translates to a net issuance of RM85 billion in government bonds. This is RM20 billion lower compared to the previous year.

Additionally, government guarantees (GG) are expected to remain unchanged, primarily due to the absence of any new major infrastructure projects as well as a commitment to financial prudence in managing off-balance sheet items by the government.

A lower government bond supply profile, coupled with sustained demand provides a favourable backdrop for Ringgit bonds especially in terms of technicals.

As developed markets approach their peak cycle, risk appetite is expected to return to the EM space which will benefit the local bond market as foreign investors are still underweight Malaysia bonds. Foreign investors have also been encouraged by recent fiscal measures aimed at optimising government spending and narrowing the fiscal deficit.

Furthermore, there is strong support from real money investors such as institutional players that should provide a buffer against any potential rise in yields. This is especially with the various Employees' Provident Fund (EPF) special withdrawals during COVID now firmly behind us.

Equities | Better Policy Clarity

One year since the formation of the unity government, we see improvements in the domestic landscape with pollical stability and major ramp-up in policy implementation.

The rollout of sound policies such as the National Energy Transition Roadmap (NETR), New Industrial Master Plan (NIMP) and a planned Johor - Singapore Special Economic Zone (SEZ) would help lay the groundwork for sustainable growth as well as provide a clear narrative of the country’s economic direction to global investors.

The recent cabinet reshuffling was also well received by the market. The appointment of an experienced technocrat to the role of Second Finance Minister as well as the return of several credible individuals to helm crucial ministries bodes well for the government’s reform agenda.

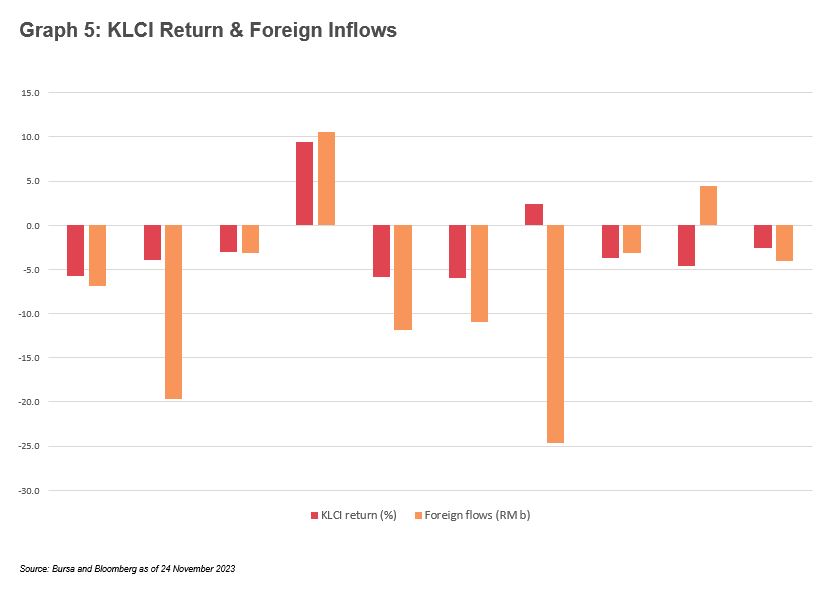

What is important now is to see a follow through on policy execution that could drive foreign inflows into the market. There have been encouraging signs pointing to a return of foreign inflows since July 2023 thanks to an improving domestic macro situation.

Historical pattens suggest a strong correlation between KLCI returns and foreign flows as seen over the past 10 years. The only exception was in 2020 and 2022 due to outsized performance by glove stocks during the pandemic which caused the divergence.

Another key catalyst for the local market is corporate earnings which is expected to recover from a low base. The rebound comes as corporates move past some of the most challenging headwinds such as COVID lockdowns and adjustments in the minimum wage and electricity tariffs.

Amongst the key thematic focus for our domestic portfolios include:-

Property: The property sector having gone through a prolonged downcycle is poised for a recovery next year supported by healthy economy and low unemployment rates. Even after a decent run-up this year, we see strong upside as sector valuation remains way below its heydays.

Renewable energy: Our positive view on is underpinned by the National Energy Transition Roadmap (NETR). The new framework is a win-win for all stakeholders as it presents a solid economic case for all players and drive demand for renewables.

Income: Within the income bracket, we see opportunities in Banks, REITS and Telcos which offer attractive dividend yields to generate a stable income stream for our portfolios.

Healthcare: Ageing population and rising insurance penetration are structural drivers for private healthcare services. Additionally, we see room for earnings upside as previously delayed elective surgeries return alongside medical tourism.