3. A bona fide inflation hedge

With inflation expected to remain higher for longer, listed infrastructure’s bona fides as a genuine inflation hedge looms large. As stated earlier, cash flows and revenues from the use of these assets are typically linked to and protected by regulation, concession agreements and long-dated contracts that may include various forms of price adjustments to help pass through the effects of inflation to end consumers.

Consequently, the returns of user-pay infrastructure companies as well as public utilities are positively correlated with inflation.

Combined with steady demand for these essential services, infrastructure companies are typically able to ensure that nominal earnings keep pace with inflation.

Put simply, we believe demand inelasticity and the ability to pass the effects of inflation to the end customer somewhat insulates user-pay infrastructure companies and utilities – and by extension investors – from the impact of inflation.

4. Underpinned by Secular Trends

Significant decarbonisation efforts in the race to net zero and shifting public spending priorities towards greening infrastructure will boost infrastructure assets.

Continued urbanisation and expansion of the middle-class will also continue to buoy the prospects of listed infrastructure assets in the years ahead, as governments ramp-up spending.

Trillions of investment dollars will likely be directed to this sector in the years ahead as global decarbonisation efforts ramp-up.

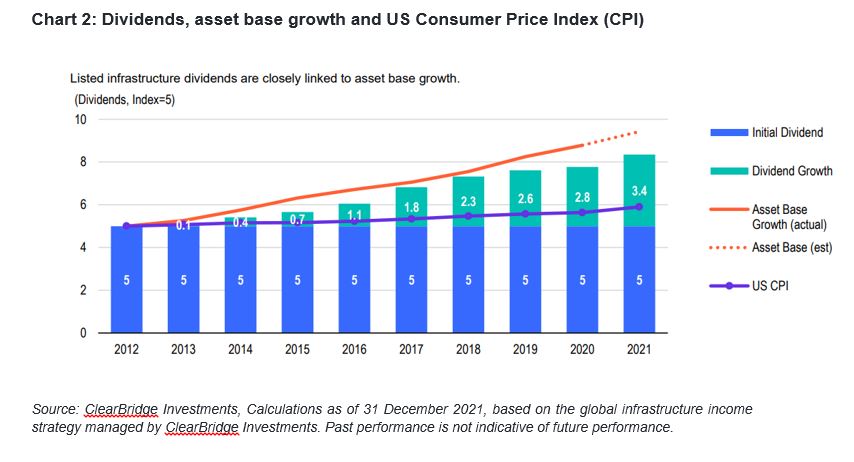

These investments will likely expand the asset bases of infrastructure companies within an environment of regulated returns, thereby allowing them to grow dividends over time.

Build Portfolio ResilienceWith little overlap against traditional asset classes such as equities and fixed income, infrastructure assets provide an additional source of diversification to investors through a stable income stream owing to the long-term contractual nature of the assets.

The Affin Hwang World Series – Global Infrastructure Income Fund provides investors access to global income opportunities through listed infrastructure assets to build resilience in their portfolio.

visit

www.aham.com.my/BUILD to learn more.