2. Understand your Time Horizon and Risk

Your current age and expected retirement age will help lay out the initial foundation of your retirement plan. If you have many more years before hitting retirement, you’ll have a longer time horizon and should be able take more risk in your portfolio.

For example, if you are 30 years old and plan to retire at 60, you have a reasonably long-time horizon. Your retirement portfolio should then be tilted towards riskier asset classes like equities which provide long-term growth opportunities.

Conversely, if you only have 5 years to retirement, your portfolio should be geared towards income and capital preservation. Fixed income which provides more predictable returns through a stable income stream should then form the majority component of your portfolio.

3. Target Shortfalls and Invest Consistently

After the above steps, you should now have an idea of how wide the gap is between your current retirement savings and your target. No matter how wide the shortfall, don’t be deterred and continue to build your nest egg by staying consistent in your investment contributions.

It may be necessary for you to increase your monthly savings rate into your retirement fund, if you are behind schedule. But, some useful tips here could be to cut back on spending and eliminate debt especially personal loans that have high interest rates. These can make a huge difference in your monthly budget and also optimise your financial habits.

When you get your salary, remember to always pay yourself first before you spend it on anything else. One way here is to automate your savings or create a direct debit order to channel your wealth towards your retirement fund regularly. Your future will definitely thank you =)

4. Plan for Medical Expenses and Contingencies

The cost of healthcare in Malaysia has steadily risen over the years because of medical inflation. You can be in the pink of health but an unexpected illness or medical condition can be enough to wipe out your entire retirement savings. Be sure to assess your insurances coverages to ensure that you are well protected.

No matter what age you are, it is also prudent to build an emergency fund which can act as a financial safety net in case of any sudden job loss or accidents. If the last few years have been any reminder, our lives can be totally upended by circumstances beyond our control like COVID.

5. Stick to the Plan and Monitor Periodically

As markets ebb and flow, you might see fluctuations in your retirement portfolio as conditions turn more volatile. But it is important that you stay disciplined and continue to invest regularly to stay on-track towards achieving your goals.

Volatility is part and parcel of investing, after all. But this is where diversification comes in as a risk-reduction strategy to help smoothen returns by offsetting losses in one asset class with gains in another.

It may be productive to also revisit your retirement portfolio with your wealth consultant at least annually for a quick progress-check. There might be a need to rebalance your portfolio to ensure that it reflects your latest risk capacity and goals.

Start Your Retirement Journey Today

A good retirement does not come by accident, it is planned with purpose.

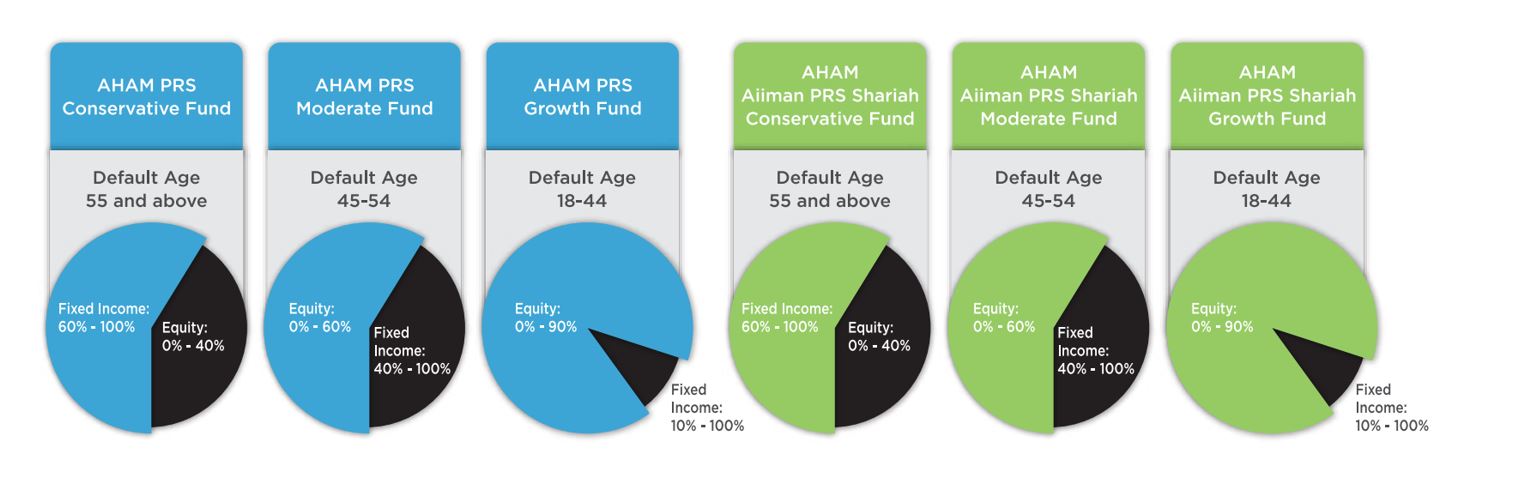

Let AHAM Capital be your wealth partner in your journey towards achieving your retirement goals. We offer a range of Private Retirement Scheme (PRS) Funds that cater to different risk appetites and ages.