All 435 seats in the United States House of Representatives (lower house), 35 of the 100 seats in the United States Senate (upper house), and the office of President of the United States will be contested when elections are held on the 3rd November.

Market Impact

There are different permutations as to how markets could potentially react in the wake of US elections.

Scenario 1: Trump wins

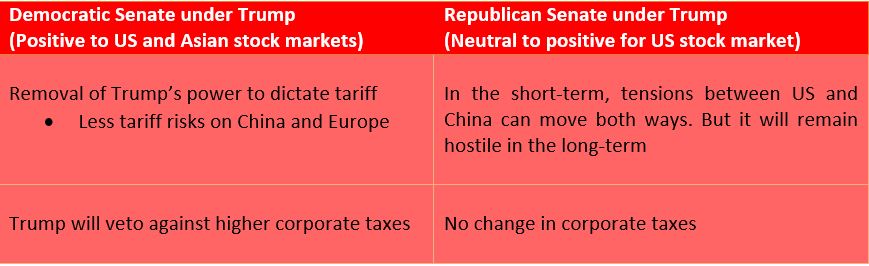

Assuming Trump takes back the White House, it will be important to also note which party gains control of the Senate that acts as a check-and-balance of the president’s power. Currently, the Republicans control the Senate and the Democrats dominate the lower house of Congress.

If the Democrats can wrestle control of the Senate from the Republicans, we could see Trump’s power being curtailed which would help rein in the mercurial president. In terms of market implication, we could see a toning down of US-China geopolitical tensions, as Trump can no longer impose tariffs on a single whim.

The Democrats which favour a rise in corporate taxes has also less chances of doing so with Trump as president who can veto against the decision. This permutation effectively keeps both sides in check that would be positive for risk assets in US and Asia.

Under a scenario where Trump is re-elected and the Republicans retain control of the Senate, it would be status-quo in the political realm and that would be neutral for the US stock market.

Scenario 2: Biden wins

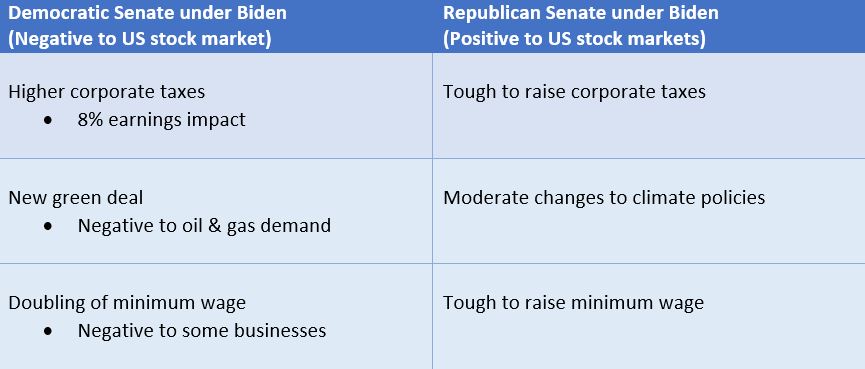

In a scenario where Joe Biden becomes president and the Democrats take control of the Senate, the US stock market could see some weakness in the short term. By adopting a more progressive tax policy, the Democrats could impose higher corporate taxes that could dilute earnings. The Democrats have also proposed to double the federal minimum wage which will impact certain key sectors.

However, any downside would be offset by a temporary moderation in the US-China trade war. With ample experience in politics, Joe Biden would likely exercise more caution and pragmatism in making policy decisions. While the Democrats would still maintain a tougher stance towards China, there is more room for consensus building and negotiation with Biden at the helm.

In another situation where Joe Biden becomes president but the Republicans retain control of the Senate, it would be a relatively better outcome for US equities. With the Republicans dominating the upper house of Congress, we could see strong pushback against any proposed increase in corporate taxes or the minimum wage. Whilst, Biden does hold some executive powers to override some decisions, there are limitations as well.

US-China Strategic Distrust Remains

Irrespective of who wins this year’s elections, a return to ‘normalcy’ in US-China ties is unlikely and will continue to be driven by long-term structural trends. China’s growing influence and trade dominance in the global stage have drawn suspicions of both the Democrats and Republicans who have found common ground in terms of their distrust of China.

We could see further ongoing economic decoupling between US and China especially on the technology front. Recently, we have seen sanctions imposed by the Trump administration that restricts any foreign company from exporting chips made using US technology to Huawei. Such moves would curb China’s technological ascension.

Manufacturing reshoring will also be ramped-up as production is brought back to the US. COVID-19 has accelerated this trend as the pandemic has revealed weaknesses in its manufacturing capacity. This is especially concerning crucial production personal protective equipment (PPE) and active ingredients used in drug production.

Post-election, we also expect more pump-priming and higher infrastructure spending in the US that will help stimulate growth in its economy.

Given the intense coverage of this year’s elections in a highly polarised environment, we can expect stock markets to surge in volatility as election looms closer. Any possible dispute in the US election results may also prolong volatility.

Investors would do well to stay focused on their goals, remain diversified and not make extreme bets in their portfolio. Geopolitics are not the only factor that can drive stock markets.

Stock markets have survived and thrived throughout countless elections in history. For example when Trump won the 2016 election, many market strategists expected a decline in stock markets. Instead, stock markets rallied after the election.

It is far more important to stay disciplined and avoid timing the market around the muddled realm of politics.