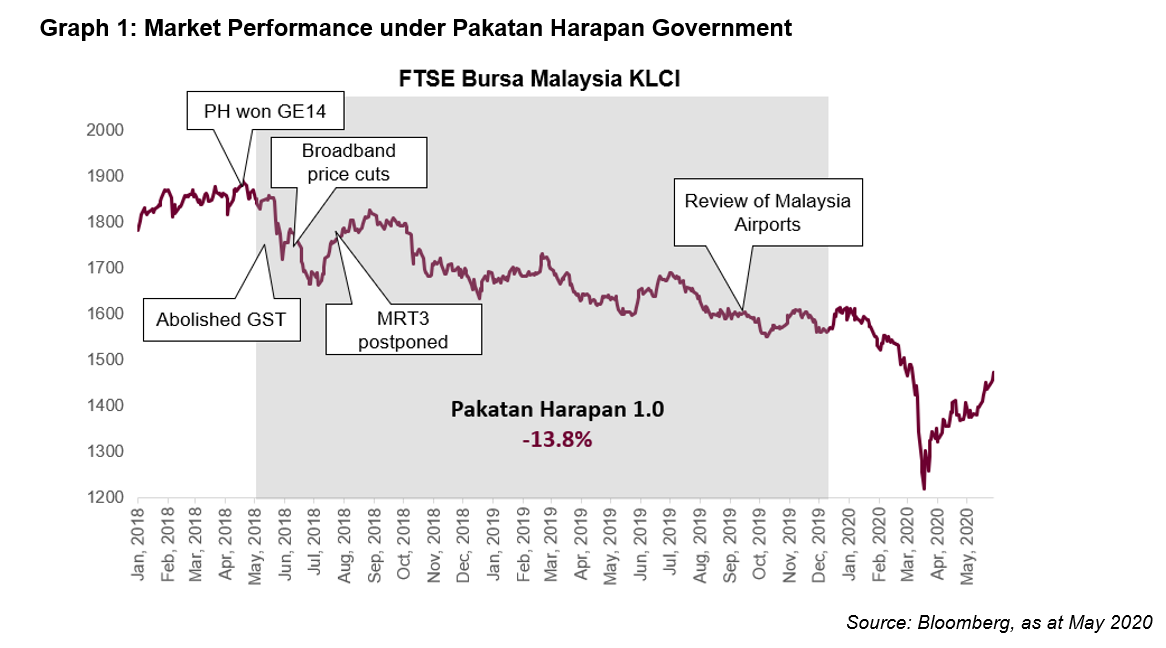

Other populist moves to abolish the goods and services tax (GST) which resulted in a RM40 billion revenue shortfall as well as broadband price cuts also decimated markets as investors grew concerned of other socialist policies.

With a second shot at power, PH is unlikely to repeat the same mistakes and policy flip-flops that plagued its first tenure especially with Anwar now firmly holding the reins. Channel checks with party officials also reveal an acknowledgement of the need to be more practical and nuanced in setting policy direction as well as communicating them.

Portfolio Positioning

Incremental positives domestically as well as in the macro environment with tentative signs showing US inflation peaking could signal an inflection point for Malaysian equities as the Fed tones down its hawkish rhetoric.

A renewed zeal to carry out reforms and to avoid repeating the same mistakes also augurs well for the unity government as it finds its footing.

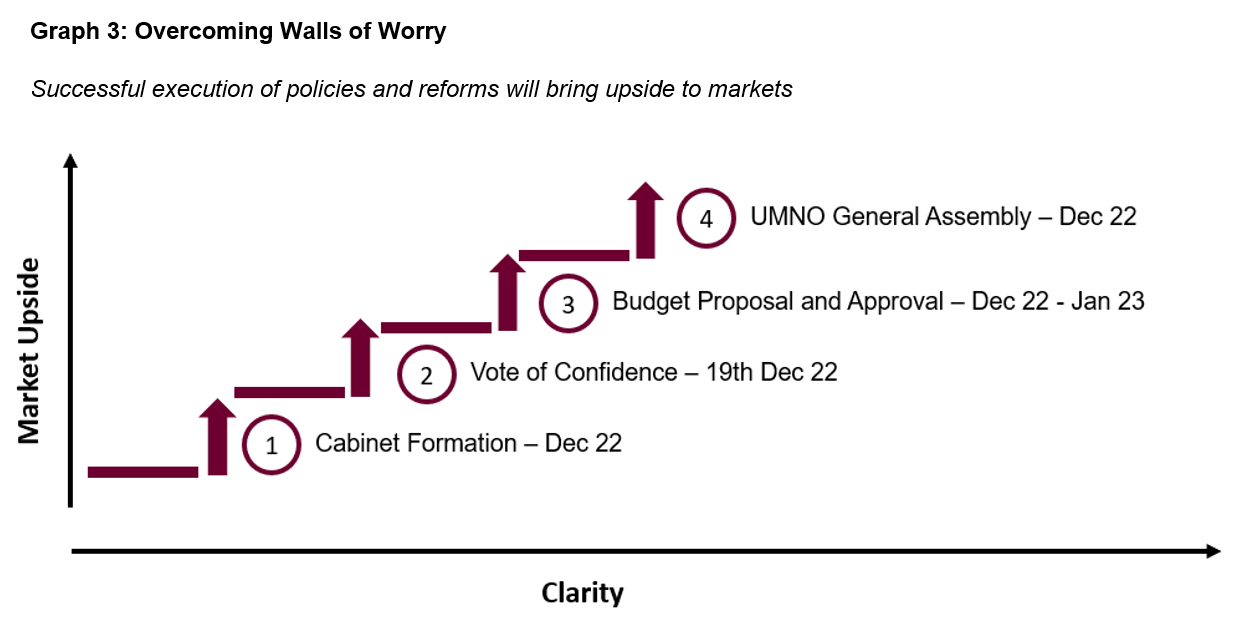

While recognising that there is a timing trade-off between waiting for more clarity but also potentially missing out on gains, we find the balance of risks tilted towards the upside.

We are taking a selective approach towards building exposure through large caps in particular:-

- Banks which continue to offer attractive dividend yields;

- Property stocks as a potential investment cycle play;

- Healthcare names given potential doubling of budget spending here;

- Beneficiaries of labour shortage restructuring;

- Beneficiaries of Ringgit strength and subsidy restructuring and;

- Reopening-plays as more cross-border restrictions are lifted