Dovish/Hawkish

These terms are often used to describe monetary policy decisions. A central bank that is dovish supports low interest rate environments in favour of expansionary growth. Conversely, a hawkish central bank supports higher interest rates to keep inflation in check to prevent the economy from overheating.

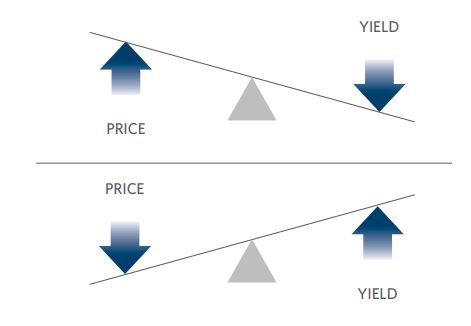

Duration

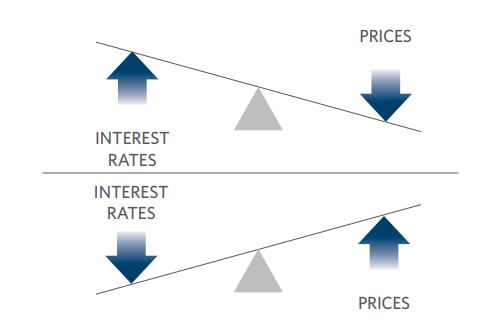

Duration is a measure of the sensitivity of the price of a bond relative to a change in interest rates. This is an important measure because the longer the bond’s duration, the more sensitive it is to movement in interest rates.

For example, a bond portfolio with a duration of 10 years tends to suffer a larger drawdown in the event of a rise in interest rates compared to a portfolio with a duration of just 1 year.

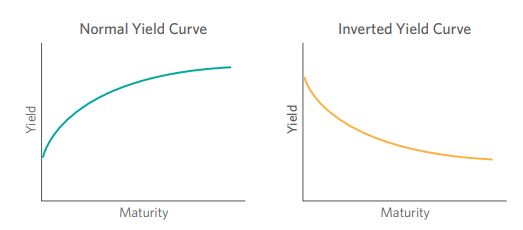

What is a yield curve?

A yield curve is a graph that plots the yields of bonds across differing maturity dates. Depending on the shape of the yield curve, it may tell us different things about what bond investors are thinking about growth and inflation expectations or interest rate changes.