In the following interview Esther Teo, Director of Fixed Income, Affin Hwang Asset Management shares her outlook for the Asian bond market as conditions start to ease after a turbulent 2018 and why credit selection is key in a late-cycle.

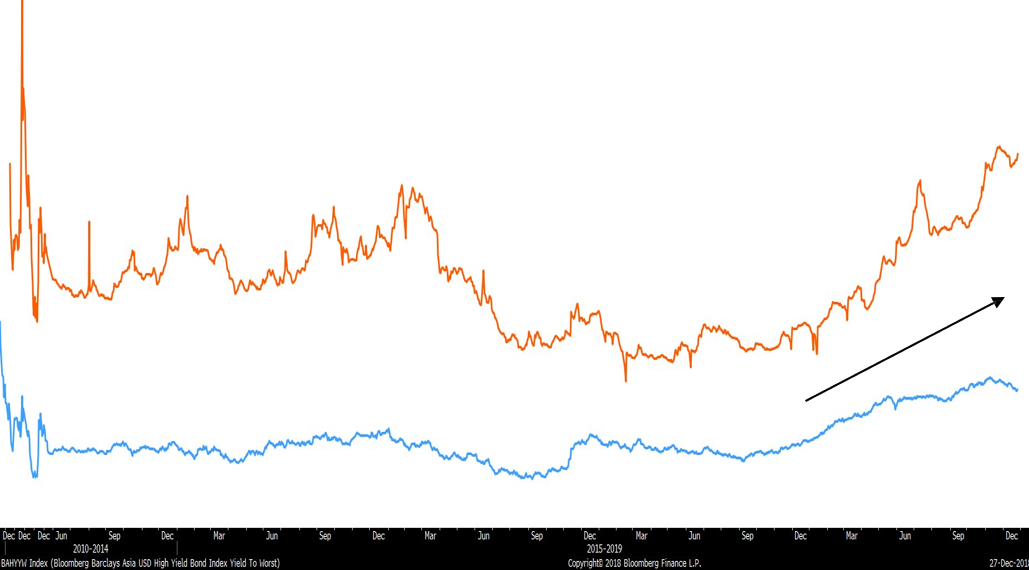

1) What are your expectations and outlook for the fixed income market in 2019? The global fixed income space endured a challenging stretch over the past year as the US Federal Reserve continued to hike rates in 2018. Emerging market bonds sold off sharply due to a surge in the USD and specific EM country currency crisis such as in Turkey and Argentina, which prompted a reversal of flows from EMs back to the US. Heightened trade tensions between US and China also dampened sentiment in the region.

Looking forward to 2019, we expect to see some of these headwinds recede as we approach the end of the tightening cycle. More dovish comments from Fed Chair Jerome Powell suggests that the central bank would be more patient and accommodative in steering its rate-hike cycle and unwinding its balance sheet.

Currently, Fed funds futures are pointing towards zero rate hikes for 2019 and a chance of a rate cut in 2020. We expect fixed income to deliver positive returns in 2019 and we see attractive valuations in EM bonds. We also expect EM currencies to be more stable as USD strength is near its peak.

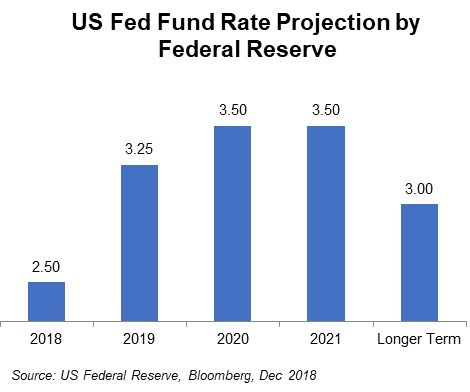

Downward Revisions Expect downward revisions in rate projections:

- Fed Funds Futures pricing-in a pause to tightening in 2019

- Core inflation to hover +/- 2%

- Narrowing growth divergence between US and the rest of the world