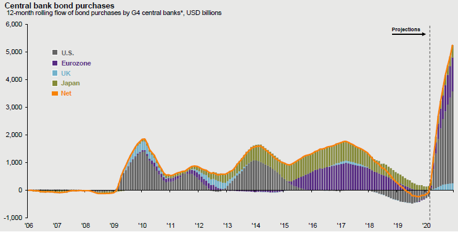

Source : JP Morgan, as at 31st March 2020

Whilst, we could see risks of defaults and credit downgrade rising as issuers face strain over their cashflows and struggle to repay debt, this is partly mitigated by a volley of fiscal and monetary stimulus measures by governments and central banks that collectively exceed US$8 trillion globally. Various forms of wage subsidies, loan guarantees and quantitative easing programme can help issuers stem the tide and recover from this economic shock. The fixed income market have also priced-in some of these downgrade risks that lay ahead which would cushion downside.

In such an environment, it is imperative to stick with quality and resilient names to weather through this period. Internally, our robust investment process will continually assess the macro landscape and stress-test the holdings in our portfolios under various scenarios to give a true picture of their credit profile.

Economic recovery will be gradual as we see various countries start to ease lockdowns and return to a new-normal state. However, strict social distancing measures in place would prevent business and activity levels from returning to full-scale, without an effective medical treatment or vaccine available.

Importance of Fixed Income

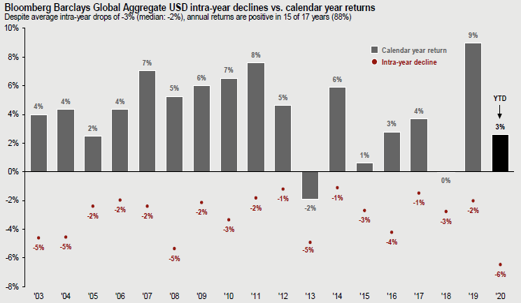

With market volatility here to stay, the role of fixed income as a defensive asset class has gained its stature by providing a measure of stability in one’s portfolio. With lower drawdowns in bond prices compared to equities during periods of market turbulence, fixed income can help cushion losses during a downturn given its low correlation to other asset classes. In 24 years of negative equity returns, bonds have stayed resilient and only posted 3 negative years in the period. Bonds have also never had 2 years of consecutive negative returns.