Unit trust funds offer investors a diverse range of investment options and among these choices is whether to opt for a hedged or unhedged currency class. Each option comes with its own set of advantages and considerations.

In our latest Fundamental Flash, we'll delve into the differences between the two and explore which to choose each based on your investment goals. But before that, here’s a look at why currency matters to an investor’s portfolio.

Same Market, Different Results

Currency volatility can play a significant role that influences overall performance returns. Given the heightened movements in currency markets, it is crucial for investors to adeptly manage currency exposure within a portfolio.

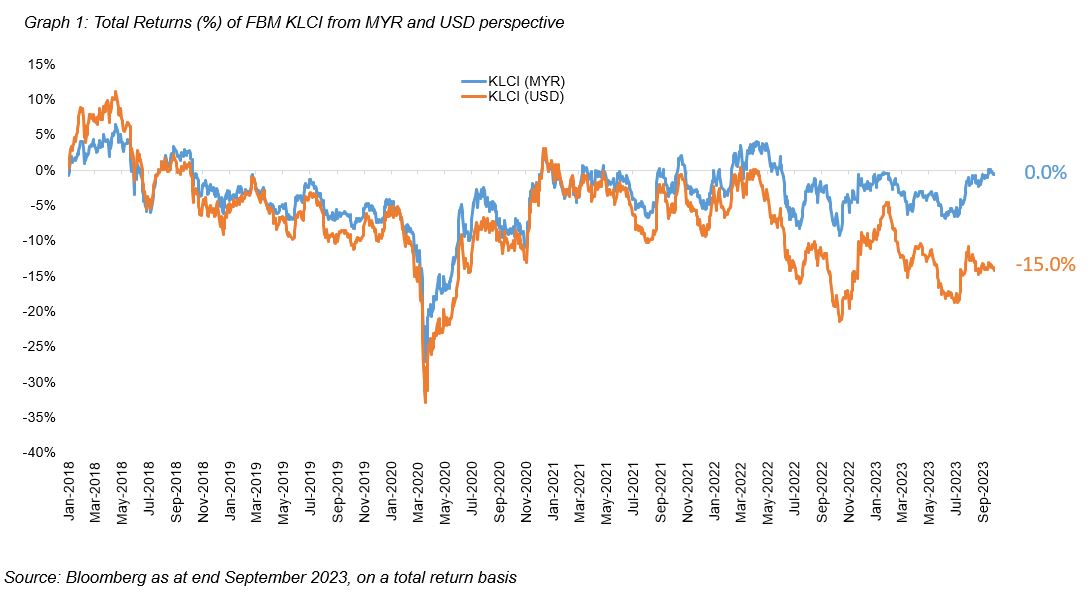

Graph 1 illustrates the substantial disparity in total returns for the benchmark KLCI when viewed from both MYR and USD perspectives. For example, a foreign investor participating in the local market might experience diminished returns when converting the investment back from MYR to USD, where the local currency has been depreciating against the dollar.

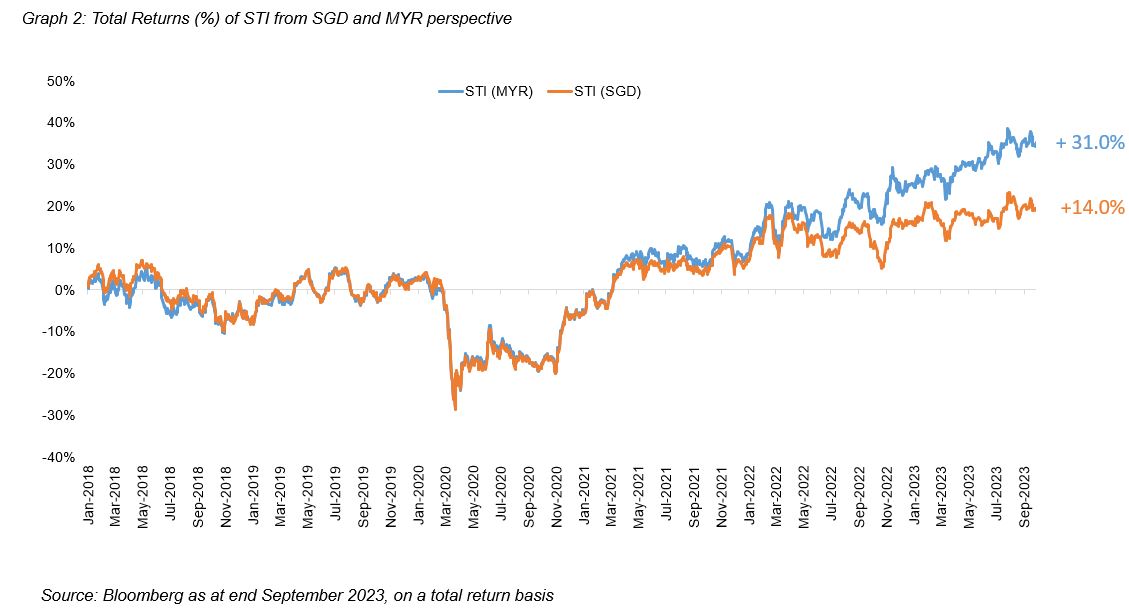

Conversely, when a local investor invests abroad and the respective foreign currency appreciates, the investor stands to gain higher returns from the investment. As depicted in Graph 2 below, a Ringgit-based investor would realise higher returns when the value of the investment in Singapore equities is converted from SGD back to MYR.

Understanding Currency Classes

Broadly, there are two currency classes investors have when investing in a unit trust fund with multi-currency options.

Hedged Currency Class: In a hedged currency class, the fund manager actively manages currency risk by using financial instruments such as forward contracts to mitigate the impact of currency fluctuations. The goal is to provide investors with more stable returns in their home currency, especially when investing in foreign assets.

Unhedged Currency Class: In contrast, the fund manager does not actively manage currency risk for unhedged currency classes. The returns are directly affected by fluctuations in exchange rates. Thus, investors in unhedged classes bear the full brunt of currency movements, whether positive or negative.

When to Choose a Hedged Currency Class

Stability of Returns: If you prioritize stable and predictable returns in your home currency, a hedged currency class is the way to go. It can help shield your investments from the volatility of foreign exchange markets.

Short-Term Investments: For short-term investments where you plan to convert your holdings back to your home currency relatively soon, hedging can reduce the uncertainty associated with currency fluctuations.

Risk Aversion: If you are risk-averse and uncomfortable with the potential for currency-related losses, a hedged currency class provides a sense of security.

Strategic Asset Allocation: Hedging can be part of a strategic asset allocation plan. For example, you might choose to hedge some of your international investments while leaving others unhedged based on your risk tolerance and market outlook.

When to Choose an Unhedged Currency Class

Long-Term Investments: Investors with a long-term horizon may opt for unhedged currency classes, as they have the potential for greater returns over time. Currency fluctuations tend to balance out in the long run, and unhedged investments can benefit from currency appreciation.

Risk Tolerance: If you have a higher risk tolerance and are willing to accept the potential for currency-related gains or losses, an unhedged class allows you to ride out currency market cycles.

Global Diversification: Unhedged classes can be beneficial when constructing a globally diversified portfolio. They provide exposure to currency movements, which can complement other asset classes.

Market Expectations: Consider the outlook for the foreign currencies in which you're investing. If you expect them to appreciate, leaving your investments unhedged may allow you to capture those gains.

Navigating Currency Volatility

The choice between a hedged and unhedged currency class in unit trust funds depends on your own unique goals, investment horizon and risk tolerance. Short-term investors may lean towards hedged classes, while long-term investors may favour unhedged ones.

Both currency classes offer unique advantages, and your decision should align with your financial strategy and time horizon. Importantly, you should consider how they fit into your overall diversification strategy to ensure that gains from one currency offset losses in another.