Investors can consider short duration bond funds or target maturity products that provide more certainty due to its fixed tenure as well as predictability of returns in a portfolio. This would allow investor to plan their liquidity requirements especially when they are in the process of de-risking.

Gold for Good MeasureGold prices shot to new highs this year breaking above the S$1,400 level for the first time since 2013 amidst recessionary risks. Other factors driving this rally were expectations of lower interest rates and geopolitical risks, with further support coming from strong central bank buying.

As a safe haven asset, gold has held a traditional role as a store of value for investors during heightened periods of market volatility and economic stress. Demonstrating resilience in times of market uncertainty, gold has the potential to lower overall portfolio volatility and increase risk-adjusted returns as a hedging instrument.

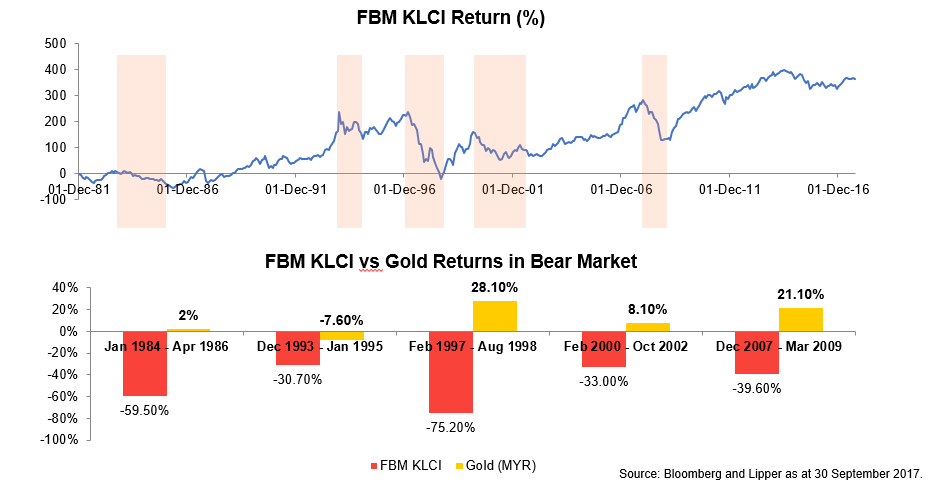

Whilst, gold is not known for its ability to generate high returns, its role as a natural hedge can grant downside protection and prevent losses from being amplified in a portfolio. Table 2 shows the performance of the benchmark KLCI compared to gold in a bear market which displays how having some gold exposure can shield losses in a down market.