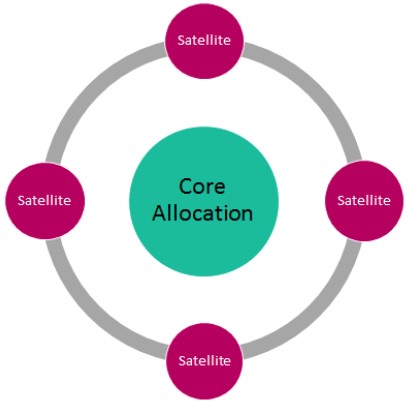

“Your core holdings would be the foundation of your portfolio composed of a mixture of growth and defensive assets. Satellite holdings are reserved for more tactical-plays or alternatives. For a risk-moderate investor, your satellite holdings could reach up to 15%. But, the core should still make up the bulk of the portfolio.” Phang says.

“The problem is when investors don’t stay disciplined and forget to rebalance resulting in portfolio drifts that deviate from the original weightage. This can result in your satellite holdings becoming larger than your core. Ideally, the gains that you lock-in from your satellite holdings should feed back into your core. That way you stay on track and your portfolio does not grow disproportionately and lead to a risk mismatch.

“My advice is for investors to also set some cash aside. Investors forget about the importance of liquidity and it serves two important purposes. First, it becomes useful for the opportunist investor looking to enhance short-term returns and deploy. And as a last resort, cash also serves as a buffer for your portfolio especially in more volatile market conditions. So, you have a safety net and some play-money set aside also. Don’t liquidate your core holdings for cash,” he says.

Achieving Ikigai

Learning to let go is a recurring theme that runs through each episode of Marie Kondo’s Netflix show as participants go through heap of their belongings and asking themselves if it ‘sparks joy’. If the answer is no, then it goes into the trash bin.

Deciding when to dispose a well-loved stock or investment can be an emotional affair for some investors. A particular stock may hold certain sentimental value and they would stubbornly hold on to them with the belief that it will continue to perform, despite red-flags pointing otherwise.

Kenny suggests that investors take a step back to look at their entire portfolio holdings objectively and find ways to consolidate. “Sometimes, it’s difficult when investors are in too fast and too deep in their position and they can’t get out. This is where a dollar cost averaging approach can come in handy to not only recoup back losses but also allow them to stay invested.”

Kenny recalls during the 2008 subprime crisis when he bought into a particular China fund which plunged to a net asset value (NAV) of RM0.28 per unit from its height of RM0.60 per unit. “I continued to dollar cost average and invest regularly even as it dropped in value. After 5 to 6 years the fund was still hovering around the RM0.40 mid-range, but by then I’ve already broke even and managed to book some small gains. In the end, the average cost came to RM0.33 per unit, as I would have accumulated a higher volume of stocks at a lower price which would bring down the overall cost of investment. If I had done nothing, I’d probably be worse off instead today. This is what we emphasise to clients to stay navigated and stay invested.”

Taking a more philosophical turn, Phang brought up the age-old Japanese concept of Ikigai that roughly translates to “reason for being.” An adage to striving for balance in life, locating one’s Ikigai can be found at the intersection of 4 dimensions. This is the perfect centre located between what you love, what the world needs, what you’re good at and what you can be paid for.