Asia Could Outperform

Against a backdrop of benign inflation and the US dollar strength topping out, Asian equity markets is expected to perform better compared to the US on a relative basis.

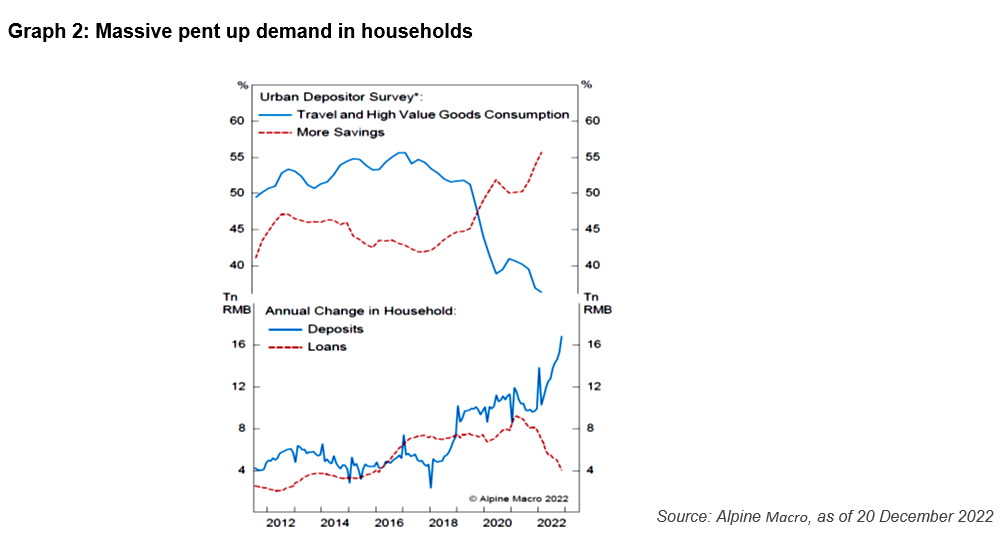

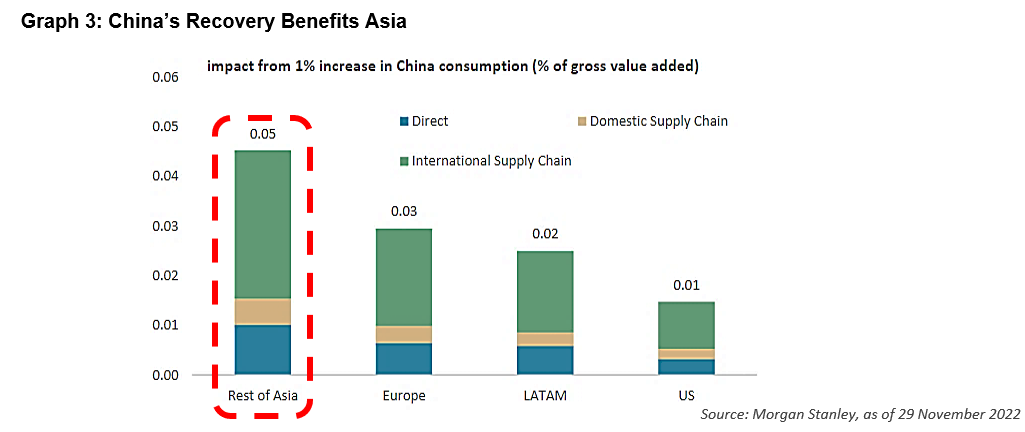

US earnings projections still appears too optimistic with EPS forecasts for 2023 only cut by 7%, while Asian markets were revised downwards by over 24%. Tailwinds from China’s reopening could also provide a lift to the region as earnings cuts find an earlier bottom.

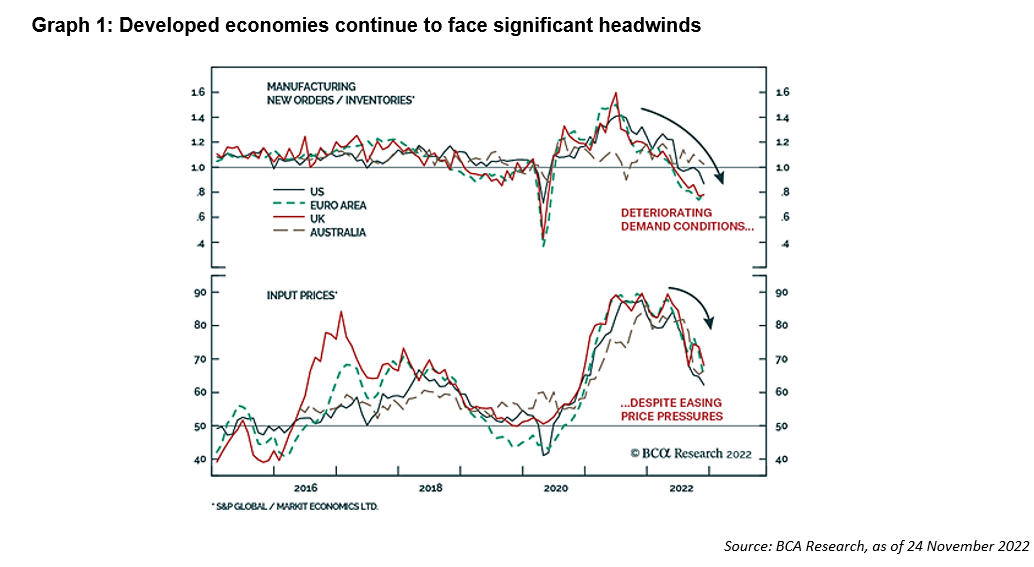

However, it will be important to monitor how deep or shallow the global slowdown will be as the impact of higher interest rates begin to bite and chip away at growth. There is also a need for more catalysts in order for Asian markets to deliver stronger upside potential.

Malaysia’s Recovery Momentum Continues

In contrast to the expected slowdown in the US economy, Malaysia’s economic fundamentals remain strong with the gross domestic product (GDP) expected to be one of the strongest in ASEAN this year. Moreover, corporate earnings is forecasted to rebound sharply, after it was dampened by a one-off prosperity tax last year.

From a fund flow perspective, domestic funds are sitting on high cash levels with foreign positioning at near all-time lows. With the return of political stability and a compelling growth story, foreign inflows that could drive markets higher. In every year between 2010 to 2021, whenever there is net foreign buying, our market has been driven positively higher.

Bonds Poised for a Comeback

Bond investors may also see some relief this year after enduring a painful 2022 which saw rates volatility reaching unprecedented highs. The US 10-Year Treasury Yield moved within a range of up to 260 bps last year compared to historical averages of 150-200 bps. In 2023, volatility in rates is expected to temper down as we see a slower pace of adjustment in rates. In addition, a slower growth outlook is beneficial for rates.

On the credit side, valuations are also turning attractive especially with higher yields which give long-term investors an attractive entry point to rebuild exposure. After massive outflows in the fixed income space, we also expect technicals to be more favourable given limited downside risks. A weaker USD environment would also be beneficial for Asian credits as the Fed slows down its pace of rate hikes.