Policy

2022 will also see major policy shifts taking place. Firstly, the US Federal Reserve is embarking on an aggressive tightening path to tamp down inflation which has surged to new highs. At a congressional hearing, Fed Chair Jerome Powell said that the Fed was determined to ensure high inflation did not become "entrenched."

Fed funds futures are pricing-in a 90.0% chance of a rate hike in March 2022 with another 3 more rate hikes expected for the rest of 2022. The Fed is also seeking to accelerate its tapering of bond purchases to shrink its balance sheet which ballooned at the onset of the pandemic when the Fed injected massive stimulus to keep the economy afloat. With inflation rising and signs of recovery in the labour market, the Fed is now thinking of withdrawing stimulus which could unnerve markets.

A key inflection point for markets to turnaround is when inflation starts to recede and the Fed becomes less hawkish in its monetary policy direction. While inflation has remained persistent, upward price pressures should start to recede on the back of easing supply bottlenecks and lower commodity prices.

Meanwhile in China, the policy focus of the government has shifted from that of regulatory tightening to now supporting growth as its economy wanes. In the past year, Beijing had cast a wide regulatory dragnet that impacted a range of sectors including technology, education and e-commerce. A slump in the property sector which is a key component of China’s GDP also dragged down economic growth.

However, Beijing is now looking to turn on the fiscal taps to prop-up growth with stimulus expected to be frontloaded in the 1H’2022. Top officials in Beijing have consistently emphasised the need for economic stability at several policy meetings last year. With a major congress taking place in 2022, there is also incentive for the Chinese Communist Party (CCP) to prevent any further slippage in growth to shore up its political legitimacy after celebrating its 100th anniversary.

Positioning

The past 2 years saw robust inflows into various asset classes including bonds and equities as investors ploughed into risk assets to ride the recovery in markets. This extended bull-run was tested several times by inflationary fears as well as supply bottlenecks, but still continued to defy expectations. The S&P 500 pierced new highs last year as investors shrug off these concerns to notch higher gains.

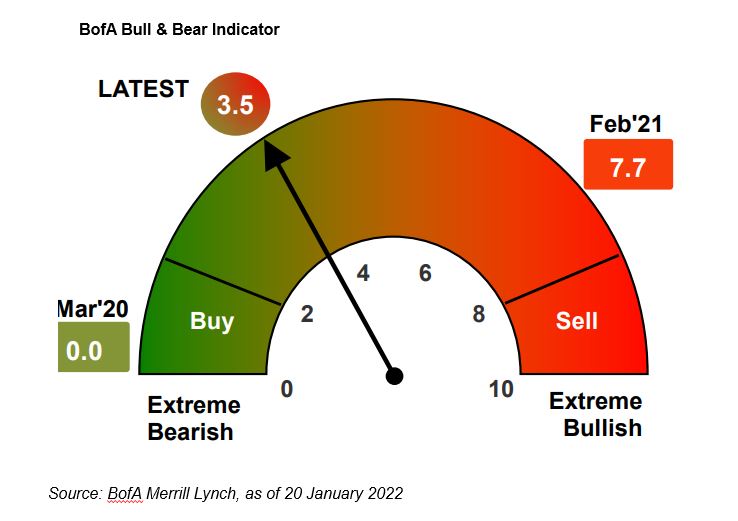

However sentiment indicators aren’t flashing irrational exuberance yet which typically portends to an imminent market pullback. In fact gauges such as Bank of America’s (BofA) Bull & Bear Indicator has fallen over the year and is sitting at neutral territory from bullish levels before.

With more favourable technicals and markets not reaching its bullish peak yet, we could see more upside for risk assets. Though, that doesn’t mean the ascent will necessarily be a smooth one with headwinds arising from higher interest rates and tighter liquidity conditions.