Pandemic & Politics

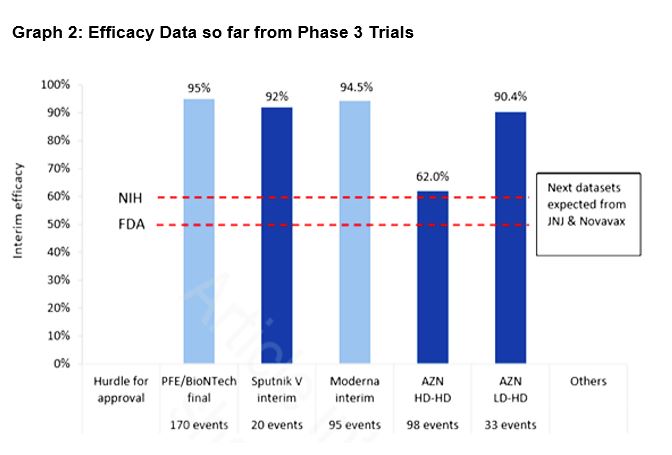

Recent progress in developing a vaccine have driven markets higher with a stronger medical arsenal to fight against COVID-19. AstraZeneca announced last month that its vaccine candidate for the coronavirus could be around 90% effective without any serious side effects, giving the world another important tool to halt the pandemic. The vaccine can also be distributed more easily because it can be kept at refrigerator temperature, unlike the drugs from Pfizer and Moderna which have to be stored frozen.

“There’s been lots of encouraging developments on the vaccine-front and we will likely continue to see more positive news coming through. Based on production guidance by these pharmaceutical companies, we can expect over 2.5 billion of vaccine shots available by late-2021.

“That is probably when deployment will be a lot more significant and we could see things normalise across different sectors and countries by 2022,” Teng adds.

On US politics, Teng believes that the biggest risk to markets is if Donald Trump refuses to a smooth presidential transition to Joe Biden. However, he notes that such a risk is now ebbing away with more clarity on the handover process.

In late November, the General Services Administration (GSA) which is a US federal agency that must sign off on the presidential transition told President-elect Joe Biden that he can formally begin the handover process. Federal resources is now being made available to Biden’s administration.

“Stock markets are staging a post-election rally as investors warm up to a Biden presidency, but a potentially divided Congress. Expectations are that the Republicans will maintain control of the Senate, thus maintaining checks and balances in terms of policy. This is an outcome favoured by markets,” said Teng.

However, he notes that tensions between US and China are likely to remain. Though, such geopolitical risk will ease slightly with Biden at the helm.

“The relationship between US and China will be better. It’s not that Biden will be taking a softer stance. In fact, he has promised to also come down hard on China during campaigning. But at least there will be consistency in terms of policy implementation.

“In markets, it is all about pricing risk. But when there’s inconsistency, the market is unable to do so and it will be extremely volatile. Biden’s administration will likely offer better clarity in terms of policy and its trade relation with China,” adds Teng.

Source: Credit Suisse, as of 23 November 2020

Political Obstacles for Malaysia

Closer to home, Teng expects the local market to stay volatile as political uncertainty cast a pall over Bursa. “Malaysia has not been a huge beneficiary of global fund inflows as seen in the rest of Asia. Foreign investors are largely avoiding Malaysia and even ASEAN as a whole due to perceived risk,” says Teng.

Market reaction to Budget 2021 has also been largely neutral. Whilst the federal budget channels large amounts of spending to vulnerable communities affected by the pandemic which is essential, the budget may not act as a catalyst for the local market, remarked Teng.

Though, he adds that it came as a relief for markets that Budget 2021 was passed at the policy stage. “If the budget was not approved, it would have sent a wrong signal to investors. In fact, we saw the Ringgit appreciate after it was approved,” says Teng.

At the time of writing, Budget 2021 is currently being debated at the committee stage in Parliament. Teng believes that there will be plenty of scrutiny to pore over the details of allocation in each ministry. “There is also some uncertainty is the budget revenue projection figures which looks to be very aggressive. The government might have to find other ways to collect enough revenue to sustain the Budget,” observes Teng.

When asked about the rubber glove sector and whether its strong performance can continue, Teng admits that most of the glove stocks have already gone ahead of their earnings cycle. Though, there could still be room for more upside if glove prices can be sustained and demand remains strong.

“The question is whether glove prices can hold up all the way to 2022? Or will glove prices start to come down? Glove players seem to think so as they see strong demand seen across their supply chain.

“The sector will likely report exceptionally good profits in the 1H’2021. If glove players can continue to exhibit strong earnings beyond that period, we could see more legs to the glove sector rally. In the meantime, it will trade range-bound. So the party may continue, but perhaps no longer as vibrant,” Teng quipped.