Step 1 - Evaluate Goals & Risk Tolerance

Financial markets and economic cycles are in a constant state of ebb and flow. However, what is even more significant is that we ourselves change and grow all the time. As we progress in our individual journeys, it is important to begin by reassessing your goals to ensure they align with your current life stage and priorities.

Have there been any significant changes, such as transitioning to a freelance career or contemplating early retirement? Perhaps you're preparing for marriage or planning to start a family. These changes can significantly influence your portfolio’s composition and how it should be recalibrated to meet these new goals.

Additionally, it's crucial to reassess your risk tolerance. As our financial situations change, so does our capacity to take on risk. Factors such as changes in income, family circumstances, or nearing retirement may necessitate a reassessment of your risk appetite.

For more short-term financial goals within the next 6-12 months, prioritise stability and liquidity by considering investments like money market funds. These instruments offer stable yields and high liquidity, making them suitable for short-term objectives.

Step 2 - Review Asset Allocation Mix

Once you've evaluated your risk tolerance and goals, review your asset allocation (e.g.50% equities: 50% bonds) to ensure that it aligns with your revised risk profile and investment goals. Consider tilting your portfolio exposure to reflect your current needs and objectives. For instance, investors nearing retirement may lean towards a more conservative allocation with a higher emphasis on fixed income for capital preservation. Conversely, those with a longer investment horizon and higher risk tolerance may opt for a more aggressive approach with a higher equity allocation.

Regardless of your chosen allocation, ensure it's one you can comfortably withstand in terms of volatility. Diversification remains a key principle in managing risk, so spread your investments across various asset classes to mitigate concentration risk.

Gold may be a great asset class to consider this year as the precious metal reaches new highs. Holding a portion of your portfolio in gold can offer downside protection during heightened periods of market volatility or geopolitical shocks. Whilst, gold should not be considered a primary driver of returns in a portfolio, its role as a natural hedge can lower overall volatility and increase risk-adjusted returns.

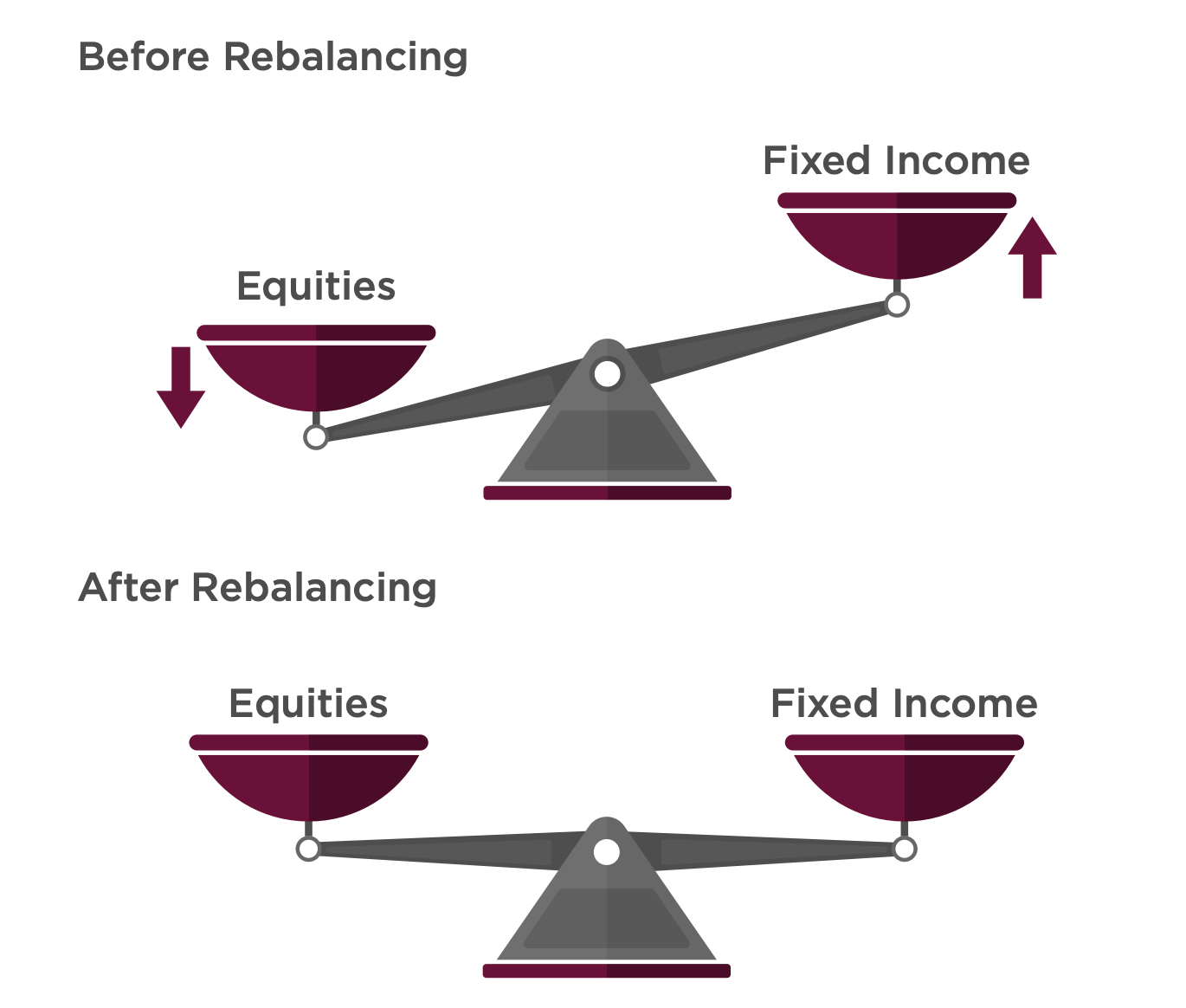

Step 3 - Review Asset Allocation Mix

Over the year, the weightage of each asset class in your portfolio may have also changed from your original target allocation. This is because of market movements that could impact the value of the underlying funds. For example, if the equity funds in your portfolio outperformed last year, then you may find that the % percentage holding of your equity funds will be higher than at the start of the year.

This could render your portfolio riskier than originally intended from a moderate level of risk, as equities are riskier compared to fixed income. Additionally, such an aggressive allocation would not be compatible with your risk profile as a conservative investor, who desires a moderate level of risk on their investments.

Thus, rebalancing helps restore the portfolio back to its target allocation and ensure that your current asset allocation appropriately reflects your investment objectives and risk appetite.

Step 4 - Assess Performance

During your mid-year review, take the time to evaluate the performance of your portfolio’s holdings to determine which has been the biggest drag or contributor to overall returns. While it is natural to glance at short-term performance metrics, it's crucial to prioritise long-term performance, typically assessed over the past 3 to 5 years.

Identifying the best and worst performers in your portfolio allows you to make informed decisions about asset allocation and potential adjustments. If certain holdings consistently underperform, it may indicate underlying issues that warrant further examination.

This could include reassessing the fundamentals of the investments, such as changes in the company's financial health or shifts in industry dynamics.

However, if your investment thesis remains intact and prices have fallen, consider averaging down to lower the cost of your investments.

An important mantra to keep in mind is to always ‘ride your winners and cut your losers’. Rookie investors often do the opposite by selling their winners to compensate for loss-making holdings in their portfolio. This disciplined approach helps prevent emotional decision-making and ensures that your portfolio remains aligned with your long-term investment goals.

Step 5 - Assess Performance

As you plan for the future, if you're feeling enthusiastic about markets and looking to juice up returns in your portfolio, you might consider incorporating a tactical allocation. This involves holding a separate portion of your portfolio dedicated to taking advantage of current market conditions or sectoral trends.

However, it's important to recognize that tactical allocation requires active management and carries additional risks. Unlike your core holdings, which are typically aligned with your long-term investment objectives, tactical allocation involves making strategic shifts based on short-term opportunities or market dynamics.

Lastly, it's crucial to maintain discipline by sticking to your investment schedule. Utilise dollar-cost averaging as a strategy to lower the purchase price of you investments over time by taking advantage of market dips as well as reducing the risk of bad timing.

Maintain a long-term perspective and keep your focus on your overarching investment goals. By adhering to your investment plan and conducting regular reviews, you can navigate the coming months ahead with confidence and resilience. Remember, successful investing requires patience, discipline, and a steadfast commitment to your long-term financial objectives.