3. China which was the first country to be hit with COVID-19 virus is seeing some signs of recovery as business activities resume. What’s your view on China’s recovery and bonds?

China remains the key engine of growth in Asia; however, the region is also supported by a number of dynamic, well run economies throughout North and Southeast Asia. The combination of a well-educated, motivated workforce, sensible economic policy, low external debt and generally decent infrastructure has created a formula of stable economic growth for the region. North Asia, furthermore, enjoys a “first in – first out” position.

Overall the default rate in the China onshore bond market is very low and is expected to stay in range. The Chinese government has been focused on achieving growth stability and implementing not only comprehensive monetary and fiscal measures, but also emergency loan programs to alleviate funding stress. All of these measures should continue to keep systemic default risks off the table.

4. In a lower-for-longer interest rate environment, where can investors find higher yield? Is it a good time for investors to look at the Asian HY space following the sharp correction?

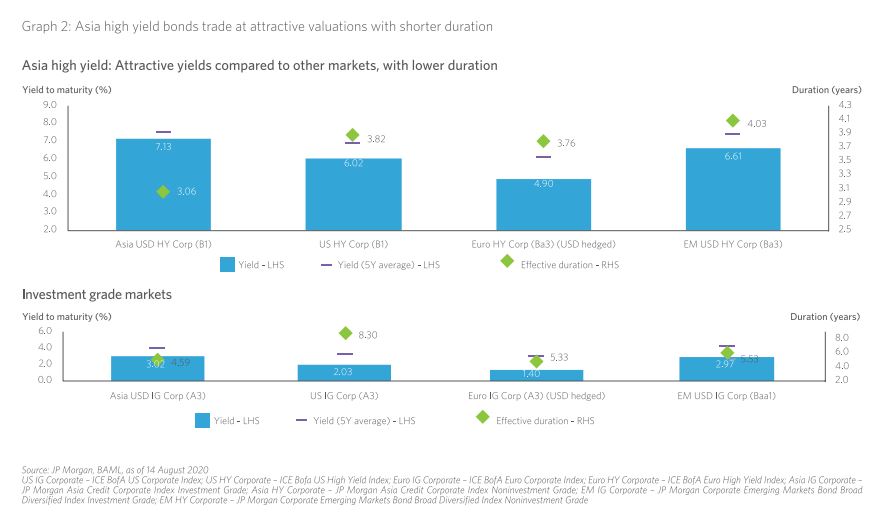

After the substantial adjustment in Asian dollar bonds earlier in the year, Asian high yield bonds have become more attractive, with the average yields at around 7.5% as of July 2020. This creates good investment opportunities in the Asian high yield bond market. On a relative basis, Asia dollar bonds continue to offer a yield premium versus bonds in the US and Europe

This is where picking the right bonds can make all the difference. With lower prices, investors have the opportunity to purchase assets at a significantly lower price. If they are able to avoid the bonds that might default, they will be rewarded with attractive potential returns later when the market recovers. And the recovery is underway.

However, there are pitfalls to look out for. A common issue facing bond markets is liquidity - the ability to buy and sell securities at will without excessive bid offer spreads. Bonds are generally not traded on exchanges and are transacted bilaterally between independent counterparties.

So when the market has more people intending to sell with very few investors wanting to buy, it is difficult to match up buyers and sellers to ensure a good two-way flow. This means that valuation prices can get marked down viciously as the clearing price in the market can be much lower than the fundamental value of the security.

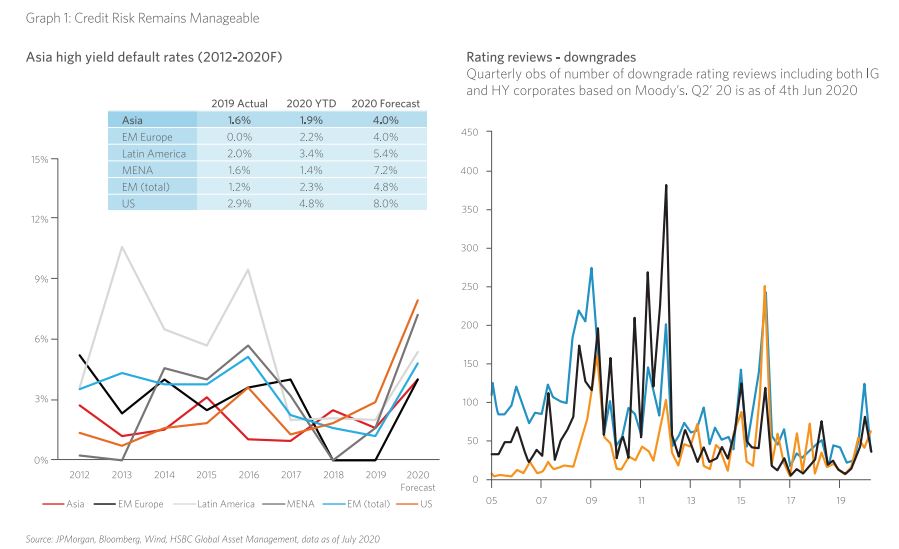

For investors searching for pockets of stronger certainty, the Asian credit market is proving to be more resilient than other markets and asset classes, particularly in the high yield space.