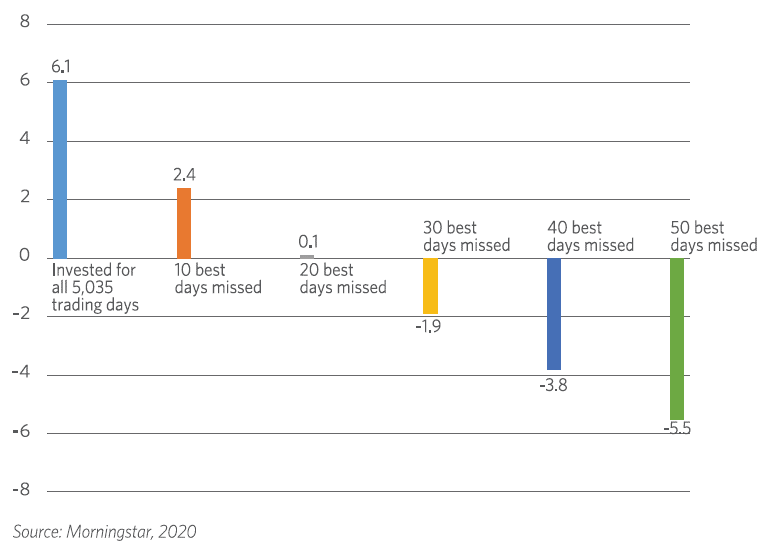

According to research by Morningstar, investors who stayed in the market for all 5,035 trading days achieved a compound annual return of 6.1%. However, that same investment would have returned 2.4% had it missed only the 10 best days of stock returns.

Further, missing the 50 best days would have produced a loss of 5.5%. Although the market has exhibited tremendous volatility on a daily basis, over the long term, stock investors who stayed the course were rewarded accordingly.

This underscores the peril of market timing that could lead to significant opportunity loss.

The appeal of market-timing is obvious by avoiding periods of poor performance to improve portfolio returns. But the truth is timing the market consistently is extremely difficult that even the savviest investor can get wrong.

As aptly put, history does not repeat itself, but it often rhymes. The COVID-19 pandemic may be unprecedented with little clarity yet on outlook, but some of the strongest rebound often occur when the market is at its most bearish.

The ideal approach to invest in such a period then is by staying disciplined and investing consistently by sticking to a regular investment plan to ease one’s way into the market.

Over the long-term, this would reduce the impact of volatility by spreading out your investments over periodic time intervals by dollar cost averaging. This ensures that one do not buy at inflated prices as well as seize the opportunity to acquire more units at lower prices.

Best Time For You, Not The MarketInstead of looking outward and trying to time the market, investors should turn inward to decide when the best time for them to invest is.

An easy way for investors to do so is by asking themselves basic financial questions such as:-

- Do I have enough in my emergency savings to cover necessities?

- What about future commitments and liquidity needs?

- Can I take a long-term view on my investments?

The global economy is undoubtedly in a fragile state as businesses grapple with closures due to nationwide lockdowns to stem the spread of the coronavirus. With companies embarking on cost-cutting measures, the likelihood of pay-cuts, redundancies and job losses may be inevitable.

That is why the importance of having enough in emergency savings cannot be emphasised enough. A rule-of-thumb is that one should have at least 3-6 months’ worth of living expenses in a rainy day fund for precisely in times like these.

Similarly, investors should also look at their time horizon and liquidity needs. Do you require cash to pay any outstanding debt or expenses in the near future? Also, can you afford to hold your investments without withdrawing for at least 3 years?

These are important points because no investment can churn out returns overnight. Patience is needed for investment success and history has proven to be kind to investors who do sit through market cycles and stay invested.

Waiting for the perfect time to invest should not be an external exercise and what happens in the market. Rather, it should be an introspective one by taking into consideration your own financial standing, investment horizon and risk appetite.