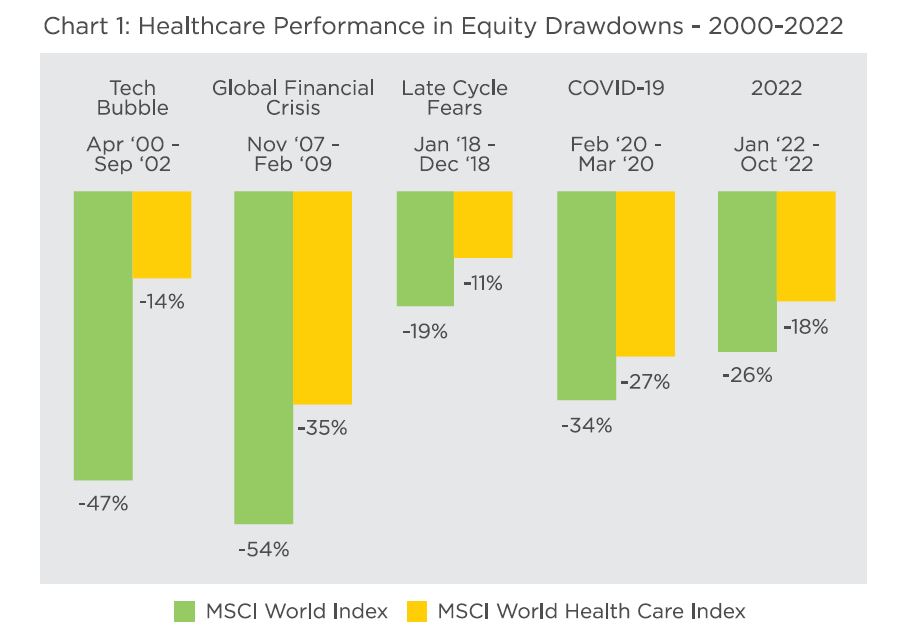

This structural demand similarly helps insulate the sector from inflationary pressures. Long term secular tailwinds, including an aging global population, further support demand in the long run regardless of the economic environment.

Pivoting from the Pandemic

The healthcare industry’s rapid response to the COVID 19 pandemic was revolutionary. The scientific strides made in a few years had a profound societal impact as the transmissibility and severity of the virus was significantly mitigated. As the acute threats of the pandemic abate, the healthcare industry seeks new applications leveraging recent innovations.

mRNA vaccines have effectively prevented the spread and reduced the severity of COVID 19 ’s evolving variants. With over 13 billion COVID 19 vaccine doses administered globally4 the demand for subsequent COVID vaccine boosters has waned.

We expect revenues from COVID vaccines to continue to decline over the next few years, but we see compelling investment opportunities for new applications of mRNA technologies.

Pharmaceutical companies such as Roche are exploring mRNA technologies to treat diseases ranging from Alzheimer’s to Parkinson’s Elsewhere, scientists at Moderna and Pfizer are researching oncological applications, including the treatment of pancreatic cancer, colorectal cancer and melanoma.

In a recent melanoma clinical breakthrough, Moderna’s mRNA vaccine, in combination with Merck’s Keytruda immunotherapy drug, was found to reduce cancer recurrence or death by 44% as compared to a treatment of Keytruda alone. Additionally, evidence suggests that the treatment’s utilisation may extend beyond skin cancer to potentially treat other types of highly mutated cancers, including lung cancer.

We continue to monitor clinical milestones, including the results of phase 3 trials anticipated in the new year.

While these innovations are positive developments, there are lingering effects of the pandemic that continue to challenge certain segments of the healthcare industry.

Labour Shortages

Healthcare staffing shortages, due in part to an uptick in early retirement following the stresses of the COVID 19 pandemic, have put a strain on hospitals and other health providers. Skilled medical professionals are necessary to carry out a large volume of medical and surgical procedures. Hospitals ‘margins have been pressured due to the higher costs of contracted medical staff that have been relied upon in replacement.

Statistics show that 1 in 5 healthcare workers in the US have left their jobs since 2020. 2 out of 3 of those who have quit decided to leave the industry entirely5.

Staffing issues have also had a detrimental impact on medical devices and supplies companies. The declining number of medical professionals available to use medical devices for elective procedures and surgeries has resulted in decreased demand for certain products.

These headwinds have brought long lasting operational deficiencies into focus. Faced with new constraints, there is now greater urgency for the industry to leverage technology to streamline processes, manage costs and enhance patient care.

Although it is our view that labour shortages have peaked and should alleviate in the next several years, we continue to explore investment opportunities as healthcare providers innovate to achieve greater efficiency.

Med Tech Outlook

Despite the labour and supply chain headwinds medical device companies have faced recently, the industry has continued to innovate and fuel attractive opportunities for growth.

Diabetes is a common affliction impacting 37 million Americans, or 11 of the adult population6. Continuous glucose monitors enable patients to manage their diabetes via real time glucose data feedback without having to endure painful finger pricks.

Medical device company Dexcom has developed a new G7 disposable sensor that is 60% smaller than predecessor models. The device, pending FDA approval, has also demonstrated improved efficacy as compared earlier versions.

Additionally, the company obtained FDA approval last year to pair its diabetes data with third party fitness trackers enabling blood sugar data to be displayed on smart watches.

Technological advances in minimally invasive procedures continue to enhance patient outcomes and present attractive investment opportunities. The technology enables smaller incisions and more rapid patient recovery times for neurosurgery, cancer surgery, endovascular and gynaecologic surgery, among others. We anticipate this market to grow over time.

The minimally invasive surgical market size was valued at US$48bn in 2021 and is forecasted to grow at a rate of 8% annually, reaching US$76bn by 20277.

Robotic assisted surgery volumes have encouragingly recovered to pre COVID levels. Intuitive Surgical, well known for its da Vinci robotics platform, continues to innovate with new integrated systems and single port capabilities designed to reduce procedural variability and enhance patient care.

Elsewhere, Penumbra has developed a physical therapy application using a full body virtual reality system Their Y Series technology guides patients through muscle and cognition strengthening activities using a virtual reality headset and connected body sensors.

The pioneering technology is designed for both physical and occupational therapy to help improve range of motion, posture, balance and cognitive stimulation.

Although these innovative developments present attractive investment opportunities, we expect certain segments of the med tech industry to remain challenged in the short-term. The recovery of medical procedure volumes has been variable. Some procedures, such as spinal surgeries, have been slow to recover and have impeded demand for certain medical devices.

Additionally, inflationary pressures and component shortages will pressure some companies’ margins through the first half of the year. We therefore favour companies with strong product pipelines and favourable earnings growth prospects.

M&A Considerations

We anticipate 2023 to be a key year for certain patent expirations. Biotechnology company AbbVie, for instance, is expected to lose market exclusivity for its best-selling anti-inflammatory drug, Humira. Similarly, Januvia, a diabetes drug produced by Merck, is also expected to lose market exclusivity in the US.

Although peak patent expiries are not expected for another few years, the threat of future declining revenues may prompt an increase in M&A activity as drugmakers seek to diversify their portfolios.

We have observed notable acquisitions recently In December, biotechnology company Amgen agreed to acquire Irish drugmaker Horizon Therapeutics for US$27.8 billion, the largest healthcare acquisition of the year. Johnson & Johnson announced plans to acquire medical technology company Abiomed for US$16.6 billion, expanding its cardiovascular business.

Separately, pharmaceutical company Merck announced the US$1.4 billion acquisition of Imago Biosciences to bolster its oncology capabilities.

We continue to monitor M&A activity and the associated impacts on companies’ pipelines and product portfolios.

Clarity on the Policy Front

With the passage of drug pricing reforms included in the US Inflation Reduction Act, there is now greater clarity following years of speculation. The legislation, passed in August, included key healthcare provisions that pave the way for future policy expectations.

Overall, we believe the potential impact of the drug reforms will be mixed for the pharmaceutical industry. On the positive side, patient out-of-pocket expenses will be capped, enhancing affordability for certain medications, such as diabetes drugs, that may result in increased sales volumes. Conversely, other drugs covered under Medicare may be negatively affected as they become eligible for price negotiation beginning in 2026.

These negotiations could result in pricing discounts ranging from 25 to 60% depending on the time since launch.

We continue to monitor these developments, headline risks and the associated effects on the companies in which we invest.

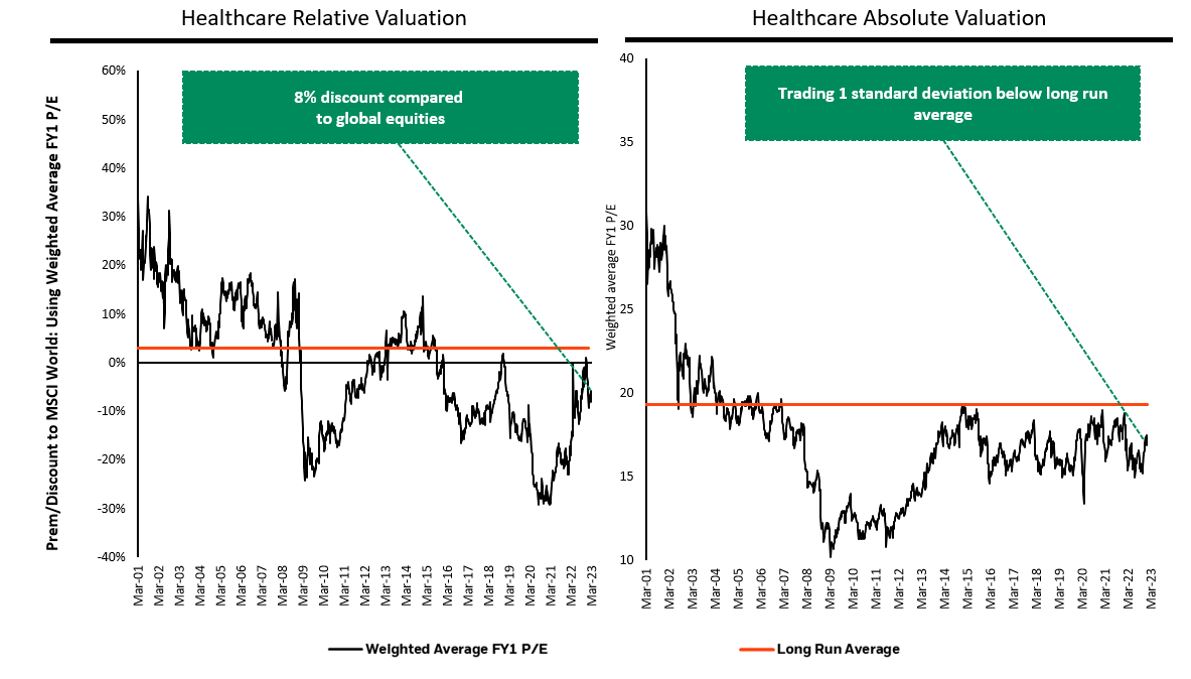

Attractive Entry Points

Valuations today for the healthcare sector remain attractive and below the long run average, with FY1 P/E ratios currently at a discount to broad global equity markets.

Within the healthcare sector, we see particularly attractive valuations among large biotechnology and pharmaceutical companies. These valuations are additionally attractive relative to other defensive equity sectors that have rallied following the recent growth to value rotation.

Investing in the Future of Healthcare

Fuelled by continuous scientific innovation, the healthcare industry presents a unique, complex and everchanging investment opportunity set. Changing demographic trends will also drive secular growth as demand for healthcare products and services continue for decades to come.

The Affin Hwang World Series – Global Healthscience Fund (“the Fund”) provides access to broad opportunities in healthcare by investing in a collective investment scheme, namely BlackRock Global Funds World Healthscience Fund (“Target Fund”).

Book an appointment with us via the link below to learn more.

aham.com.my/Book-An-Appointment