Gold is gaining its lustre this year as skittish investors make a dash for the safe haven asset amidst heightened volatility in markets.

A whirlwind of factors including rising inflation, Russia-Ukraine tensions and prospects of slower economic growth is fuelling gains in the precious metal which is flirting around its all-time high of US$2,000 at the time of writing.

With gold proving its mettle yet again as the go-to asset class in times of crisis, we explore the 3 vital roles that gold can play in a portfolio.

1. Store of Value

In a world of macro extremes where geopolitical fissures can easily erupt into a full-blown conflict overnight, gold acts as a reliable store of value for investors due to its intrinsic properties.

Beyond its sparkle and luminosity, it is also malleable, non-toxic and does not corrode making it highly in-demand amongst developed and emerging countries to make gold bars, jewellery and even electrical components.

However, the biggest net buyer of gold has to be from central banks because they store massive amounts of it in their vaults. Over 66% of the US Federal Reserve and Germany’s central bank foreign reserves are kept in the form of gold because it is seen as a medium of exchange that helps protect the value of their currencies. (Source: World Gold Council, as at 31 Dec 2021)

Gold’s value also comes from its scarcity because there is a finite supply of the commodity in the world. This is unlike paper currencies that can be printed, but then loses its value over time because there is now more money in circulation.

That’s why investors through the ages still continue to keep gold in their portfolios as a form of wealth insurance to provide financial coverage especially in a crisis.

2. Portfolio Diversifier

With a negative correlation against risk assets like equities, gold also acts an effective portfolio diversifier so that losses in one asset class are offset by gains in another. This helps shield portfolio returns especially in a market downturn, so that investors have the holding power to ride the rebound when markets eventually recover.

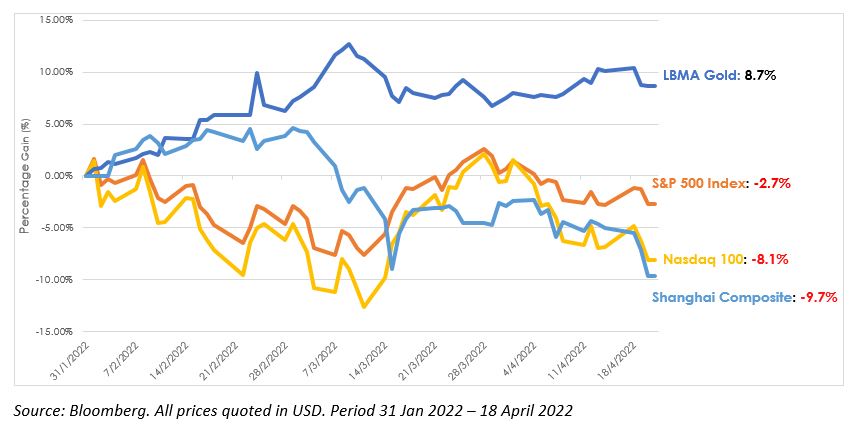

This is evident from Graph 1 below which shows a clear opposite mirror image of the price movements of gold and major equity benchmark gauges this year. It can be seen that the LBMA Gold Price index climbed 7.7%, while the S&P 500 floundered at 0.1% in the 1Q’22 as markets were jolted by escalating tensions between Russia and Ukraine as well as rising inflation.