Risk assets endured a fierce sell-off in the past month as global markets reeled from contagion fears arising from the Covid-19 outbreak. At the time of writing, the number of new infections surpassed that of China with fresh cases springing in Italy, South Korea and Iran.

Investors have been closely tracking the outbreak to assess its potential impact to the economy as a result of wide scale city and factory shutdowns, as well as travel restriction bans. Global supply chains have also seen disruption due to stalled manufacturing activity, impacting markets like Taiwan and Korea which are heavily interlinked.

The Covid-19 epidemic has quickly overtaken headlines as a black swan event that could delay an economic recovery. Indeed, markets were too quick to give the all-clear signal at the initial flare-up of the epidemic and subsequently corrected in late February again.

However, the ensuing market correction is likely overdone with volatility exacerbated by the presence of algo-traders. The washout in financial markets was so severe that it even prompted the World Health Organization (WHO) Director-General Tedros Adhanom Ghebreyesus to call for composure and said global markets “should calm down and try to see the reality.”

Telling investors to calm down may sound paradoxical, but it does allude to the irrational behaviour seen in markets especially in volatile times. Perhaps investors should heed the WHO’s advice and take a step back before following the herd?

Lessons from History

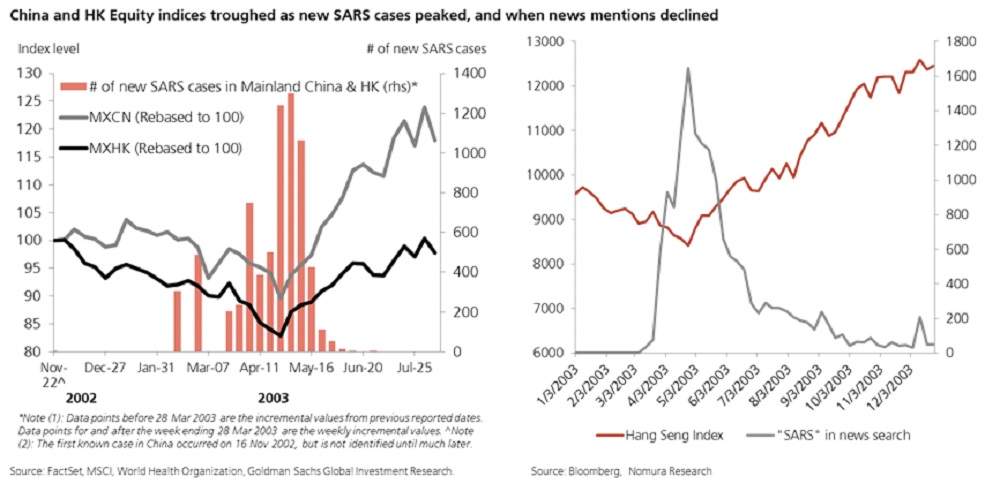

David Ng, Deputy Managing Director & Chief Investment Officer says it is worth revisiting history to understand how markets behave in past epidemics, the most recent being the Severe Acute Respiratory Syndrome (SARS) outbreak in 2003.

“The lesson from SARS is that the economy and stock markets can quickly recover once the virus contagion recedes. With more decisive measures and effective control policies by governments in containing the outbreak, we view that the global economic recovery risks being delayed rather than derailed,” said David.

Whilst the impact of the Covid-19 outbreak could last for a few quarters, David expects that the impact on stock markets will be shorter.

“Once Covid-19 recedes, we believe the global economy will bounce back as months of pent-up demand flows into the economy just like when SARS receded. We do not know when this will happen. But we suspect that Covid-19 will recede within a few quarters based on what we have learned about past viruses.”

However, the economic impact of Covid-19 is expected to be larger than the 2003 SARS outbreak given that China now constitutes a bigger part of the global economy, according to David.

“Import demand from China makes up 2.4% of global GDP today as compared to 0.4% in 2003. As such, a weaker Chinese economy today will undoubtedly affect the global economy more so than in 2003.

“Whilst we could see impact to China’s 1Q’2020 GDP, additional fiscal and monetary support may cushion downside to its economy albeit with a lag effect. The quick and measured response from Chinese authorities in containing the outbreak has also soothed fears, as authorities draw upon lessons from past outbreaks like SARS and MERS,” states David.