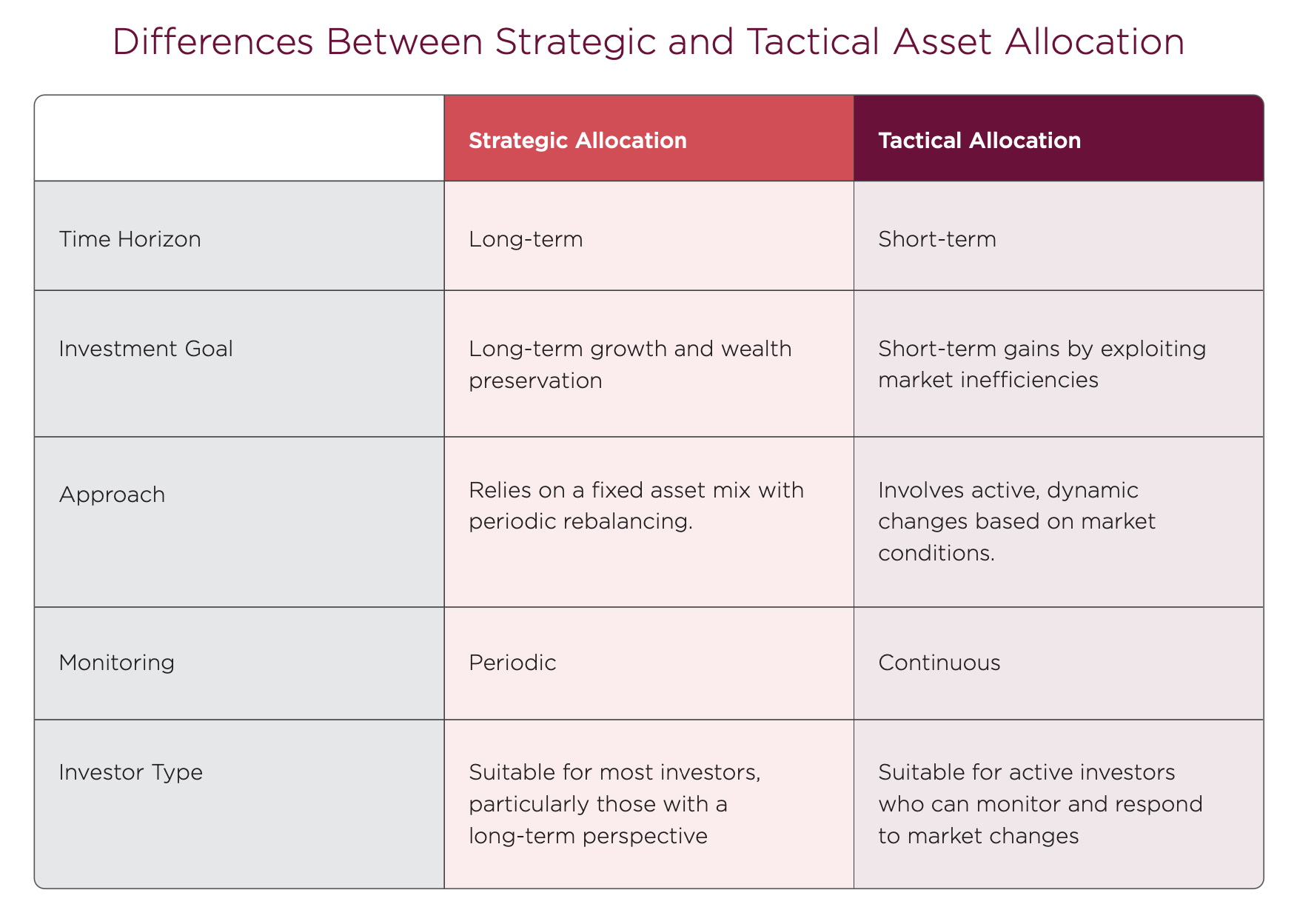

How Both Strategies Complement a Portfolio

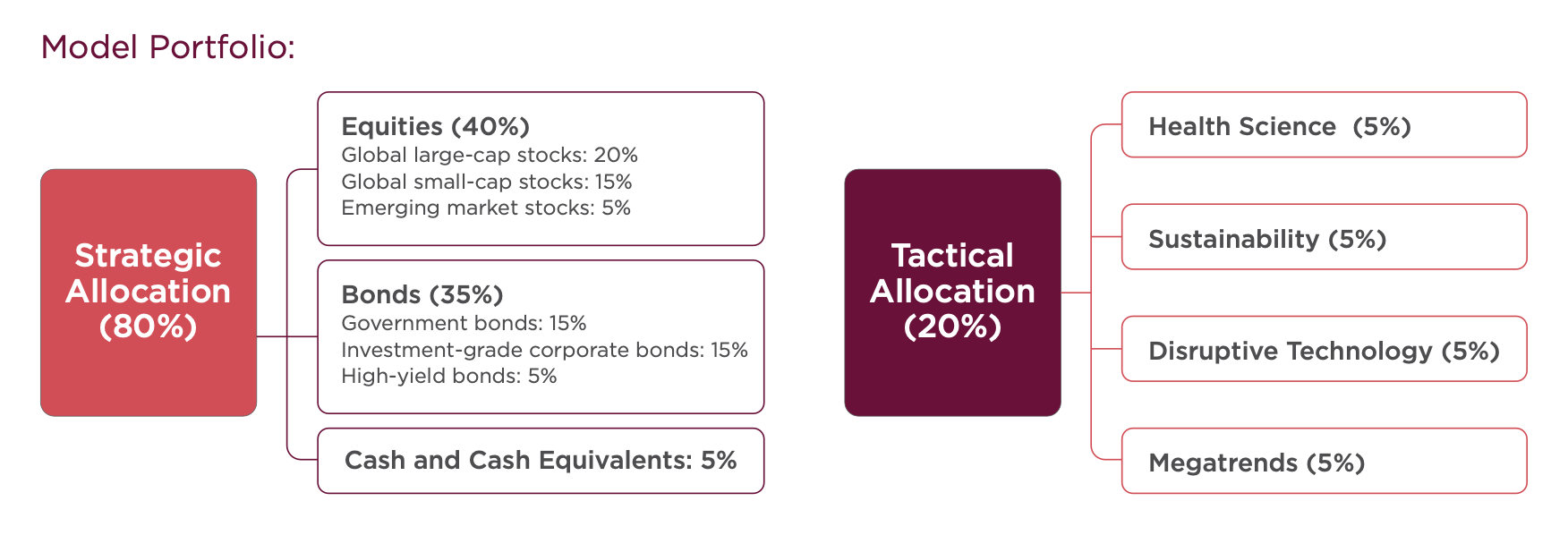

In the example above, SAA forms the bedrock of the portfolio. By committing 80% of the portfolio to broad, diversified exposure across different global markets and asset classes, investors ensure a stable and consistent approach to wealth accumulation.

For example, a balanced investor might allocate 40% to equities ensuring exposure to both large-cap, small-cap, and emerging market stocks.

Within the bond segment, the investor may allocate 35% of the portfolio across government bonds, investment-grade corporate bonds, and high-yield bonds which provide a steady income stream and help cushion losses in equities.

Additionally, having 5% in cash and cash equivalents ensures liquidity for immediate needs or as spare ammunition to deploy.

On the other end, the TAA component comprising 20% of the portfolio, is where active management comes into play. This segment is designed to capitalise on short-term market inefficiencies and emerging trends.

For instance, dedicating 5% to health science allows investors to benefit from advancements in biotechnology, pharmaceuticals, and medical devices. Similarly, a 5% allocation to thematic trends such as shifting demographics positions the portfolio to gain from changes in consumer preferences.

The sustainability allocation of 5% focuses on low-carbon investments and companies that are poised to benefit from the transition towards renewables. Finally, a 5% stake in disruptive technology, including artificial intelligence, blockchain, and robotics, ensures exposure to companies involved in groundbreaking innovation.

Complementary Strategies for a Resilient Portfolio

Strategic and tactical asset allocation are both essential tools in an investor's toolkit. While strategic allocation provides a stable foundation aligned with long-term goals, tactical allocation offers flexibility to capitalise on short-term opportunities. By combining these strategies, investors can build resilient portfolios that adapt to changing market conditions and help them reach their financial goals.