As bond yields ascend to new highs this year, many investors may find themselves sitting on cash and wary about deploying into fixed income.

Understandably, the sharp rise in yields has stirred some anxiety amongst bond investors who fear that higher yields might lead to a brief decline in the price of their existing bond portfolios.

However, adopting such a short-term perspective overlooks the long-term opportunities that arise from higher yields as well as the risks of holding too much cash for extended periods.

In our latest Fundamental Flash, we delve into why the current market backdrop might just be the opportune moment for investors to step off the sidelines and start building back exposure in bonds.

Lock in Higher Yields

Strong economic data as seen in recent consumption and production figures have bolstered the case for a soft landing in the US.

In part, this is being reflected in higher bond yields as the US Federal Reserve (Fed) is expected to keep interest rates in restrictive territory until inflation can trend downwards sustainably to the central bank’s target of 2%.

For investors who have been dissuaded from investing in bonds for years due to the low interest rate environment, the search for yield has become a whole lot easier.

With the US 10-Year Treasury yield reaching a 15-year high and piercing above the 4% level, it is no longer an environment where investors have to sacrifice returns by loading up on bonds.

Instead, investors can now lock in higher yields with certainty to generate a consistent income stream by clipping the coupons from holding the bond to maturity.

Reap Potential Capital Gains

After embarking on a rampant fire-fighting exercise to douse price pressures, the Fed’s interest rate hike cycle looks closer to reaching its tail-end in the 2H’2023.

Inflation numbers have declined from its peak. The US core consumer price index (CPI) peaked at 6.6% in September 2022 and the most recent print in September 2023 came at 4.3%. The recent inflation numbers could give the Fed some breathing room to pause and allow its series of aggressive interest rate increases of over 500bps to filter through the economy.

At its FOMC meeting in September, the Fed held interest rates unchanged as widely expected. Though, the central bank signalled that interest rates could stay higher-for-longer to bring down inflation sustainably as it keeps a close eye on data. The Fed’s latest dot plot projections showed the likelihood of 1 more rate increase this year.

As the cumulative and delayed effects of the Fed’s interest rate hikes trickle down to the broader economy, it is likely to translate into slower economic growth or a higher possibility of recession.

In periods of slower economic growth, it is worth remembering that fixed income tends to outperform other asset classes. They serve as a ballast to an investor’s portfolio due to its defensive attributes as well as a source of capital preservation.

This is especially for high quality investment grade (IG) government and corporate bonds that have historically held its ground in a downcycle.

Furthermore, as we draw closer to a rate-cut cycle that could happen as early as 2024, bond investors could find themselves in a favourable position to benefit from capital gains. Fed officials expect to make 2 interest rate cuts (totalling 50 bps) for 2024 and 2025 respectively according to its dot plot.

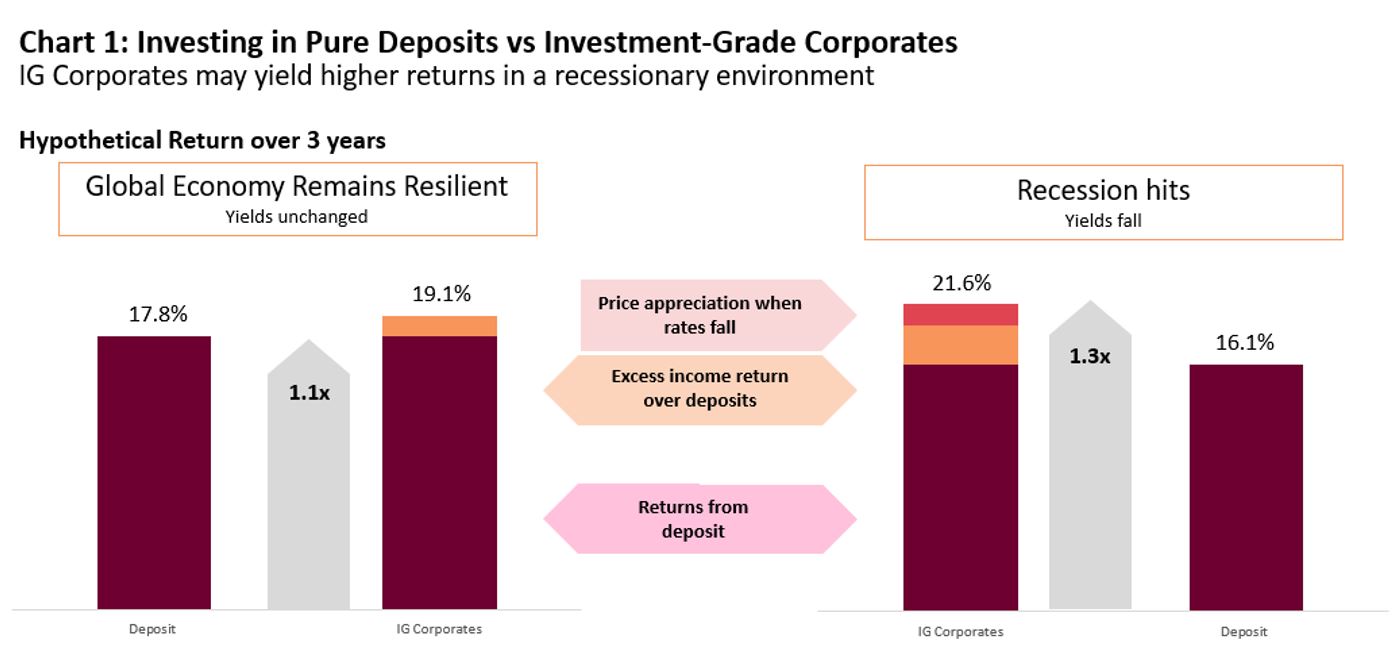

Taking a hypothetical example, an investor could make return of 21.6% over a period of 3 years (Chart 1). This return encompasses both income and capital appreciation as bond yields fall when the economy enters a recession. This more than surpasses the returns of an investor who only invested in pure deposits of 16.1%.

Hypothetical example shown for illustrative purposes only.

Data as at 31 July 2023. Yield-to-worst ("YTW") and duration figures of the Target Fund of AHAM World Series - Global Corporate Bond Fund ("Target Fund") are used as starting points for the scenario analysis to simulate returns of investment-grade corporates (“IG Corporates”), while deposits are represented by 1-Year USD placement rate from a local bank. There may be differences due to rounding effects. Returns are in USD terms. Sources: JPMorgan Asset Management, Malayan Banking Berhad.

Additional income return is the difference of YTW earned over deposits. Price appreciation is calculated using the interest rate sensitivity (i.e. duration) of investment-grade corporate bonds to a change in rates.

1. The 'stagnant rate' scenario analysis assumes deposit rates and YTW remains constant at 5.60% and 6.00% respectively for Years 1-3.

2. The 'recessionary scenario' assumes YTW falling by 0.5% when rates drop 1.0% and investment-grade corporate spreads rising by 0.5%. The deposit rates are 5.60%, 5.10% and 4.60% annually over the 3-year period. YTW used are 6.00%, 5.75% and 5.50% annually over the 3-year period. Modified duration of the Target Fund is 6.0 years and is held constant over the 3-year period.