This year has been a tough one for China equity investors. On the face of it, investors had a lot of reasons to expect a good year: the Chinese economy is doing well relative to other economies, peoples’ lives are back to normal, and production has returned. However, the reality in the markets are different from what people expected because of regulatory measures taken by the government.

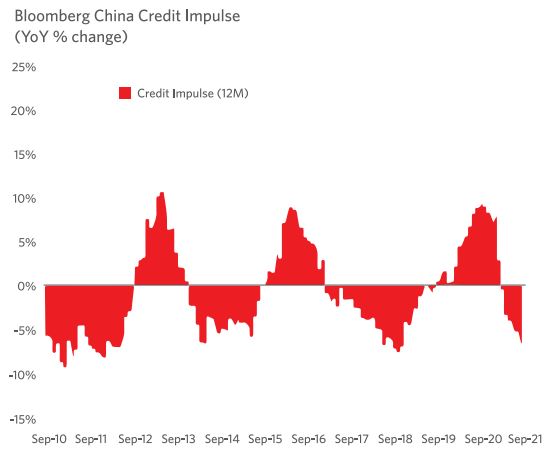

But one thing I want to bring to everyone's attention is that policy in China has cycles and the government also cares about GDP growth, unemployment, and economic stability. We've seen recent macroeconomic indicators pointing to a deceleration in the Chinese economy and we think the numbers will have some impact on the government’s mindset in fine-tuning the policies.

Even though we have already seen some signs of change in tone, it might not be enough to convince investors to come back to the market right away, but I think we probably have seen the worst and from this point on we will probably hear some positive signals from the government.

2. What is the impact of China's goal of the “Common Prosperity” drive?

When market sentiment is weak, new ideas like “common prosperity” normally lead to different types of interpretations compared to when the market is strong. My personal view is that “common prosperity” is not a policy to “rob the rich and help the poor”.

The “common prosperity” direction is targeted at reducing the gap between rich and poor, which is a common and noble policy target for many governments in the world. If “common prosperity” is focused on policies such as providing more social insurance and health coverage for poorer people, it will likely mean more sustainable long-term growth for China.

3. Why did the Chinese government choose to launch the “Common Prosperity” drive so quickly?

When the economy is doing well, the Chinese government has the confidence and consensus at the top level of policy making to attend to issues which have accumulated over the years. China’s rapid recovery from the COVID-19 situation gave the government confidence to deal with many issues, like high levels of debt in the financial systems and other social concerns.

China’s political system is top down. Once consensus is reached at the top, middle and lower-level officials must act fast to maintain the party line. So, when the policy swing happens, it feels very strong. That said, you can’t make a linear prediction and expect policies to continue tightening. The government isn’t trying to deliver a sharp economic slowdown. Once consensus is reached at the top about dealing with the slowdown, a lot of supportive measures will come out as a result.