2. What's your outlook for the Malaysian stock market over the next 6-12 months? Do you see more legs to the rally?

The Malaysian market like the rest of the world, is showing a disconnect between fundamentals and market performance. We have neutral underlying fundamentals and weak earnings growth, even without COVID-19 and political overhang in the picture. But because of global and domestic liquidity conditions, markets have done well.

Hence for our market outlook, we are focusing on the incremental changes to liquidity conditions to determine its direction. We would look for a continuation of easy and abundant monetary conditions globally to sustain this liquidity driven market.

Domestically, the expiry of the loan moratorium in September could have a significant impact, given that about RM100 billion of liquidity was added into the system between March to September; with approximately RM60 billion benefiting individuals. This partly explains the recent spike in retail investor activity.

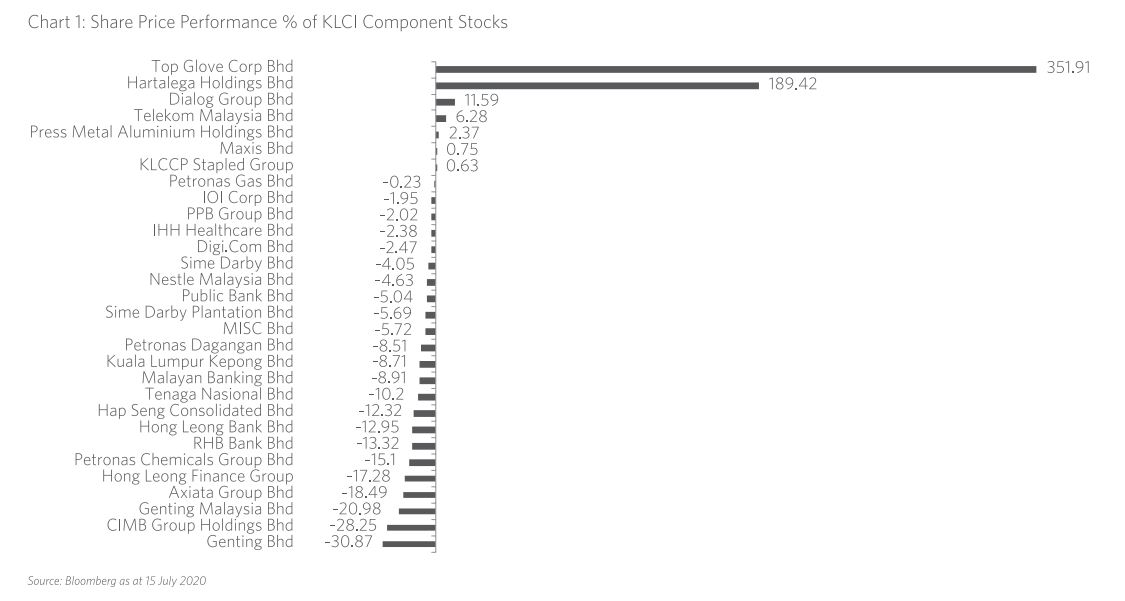

On a more micro level, the two winning sectors (i.e. gloves and technology) need to be closely monitored as they are the primary drivers of market performance. For gloves, we are monitoring retail participation, glove demand and pricing, vaccine development as well as investor expectations. For technology, we are monitoring feedback from global supply chain and the NASDAQ performance in general.

3. How are you positioning the portfolios then against the current environment?

We will continue to stay the course given still stable or improving liquidity conditions and buoyant sector fundamentals; and we would change our view when these conditions change. We realise this is rather circular in nature, but that's the nature of liquidity-driven markets.

If economic conditions continue to normalise, we would add banks, plantations, construction and other value plays for potential switch of momentum stocks into value.