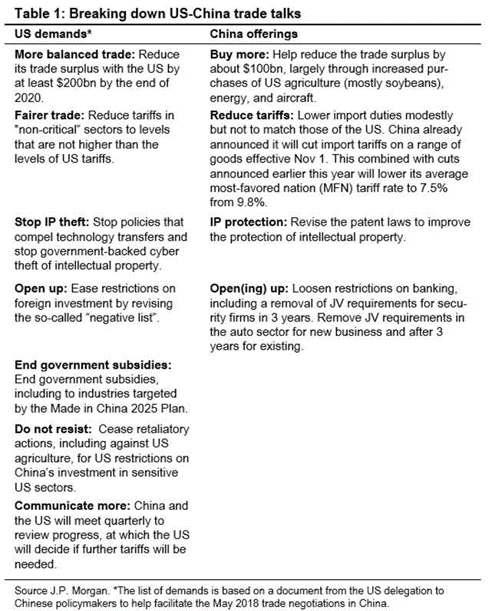

These can be thought of and placed into 3 categories – the first category is where China is willing to compromise, the second category where China is willing to negotiate and the third category is where China is not willing nor able to negotiate as these issues centre around national security or national ambitions.

The first 2 categories are relatively low- hanging fruits that can be negotiated easily, as seen recently with China pledging to narrow its trade surplus with the US by purchasing more US goods or removing barriers of entry into its domestic market in its auto and finance sector.

We believe the key barrier to a lasting trade agreement is that roughly a third of US demands on China falls into the 3rd category that are non-negotiable.

This could mean China abandoning its ‘Made in China 2025’ goals and being forced to cede its technological advancement ambitions. Any deal resulting in China compromising on this category would certainly be bad optics for President Xi Jinping and the ruling Communist Party by coming across weak and hurt the party politically.

3) We’ve seen EMs perform strongly at the start of the year on the back of a weaker US dollar and Fed turning more dovish. Do you think there are more legs to the current rally once this trade overhang is removed? Should the US-China trade dispute remain status quo or even improve, the market will have removed one point of uncertainty from the overall global growth outlook. However there are still other points of uncertainty that remain on the horizon clouding the outlook on global growth, such as the US growth momentum, global liquidity tightening, as well as political issues in Europe and the Middle-East.

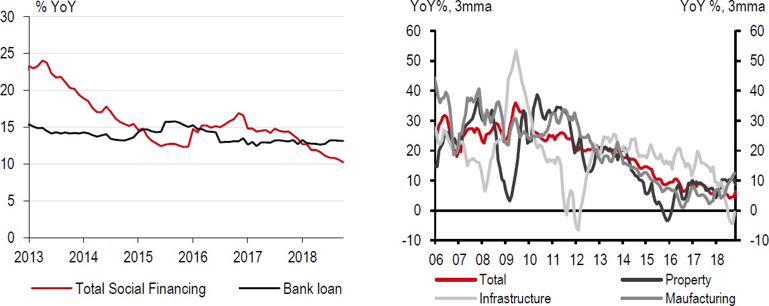

4) We’ve seen China announced a slew of easing measures to prop-up the market as growth cools domestically. What is your outlook on growth for China and will these stimulus measures be effective? Currently, the market expects that China’s GDP will grow at a slower pace than in 2018. Thus far the total effect of the announced stimulus measures when compared to those taken during 2015 and 2016 (e.g. reserve requirement ratio (RRR) cuts, special bond issuance, as well as the pace of local government debt issuance and swap), have been roughly on the same magnitude as in 2015/2016.

In 2015, China also had the tailwind of interest rate cuts and the size of the economy was much smaller and the fiscal multiplier effect of stimulus, larger. While details of more possible stimulus measures are in the pipeline and expected to be announced soon (value-added tax (VAT) cuts, stimulus measures for home appliances and autos), we should expect the Chinese authorities to abide by Xi’s emphasis on growth quality rather than speed, hence we do expect growth to continue to soften from 2018.