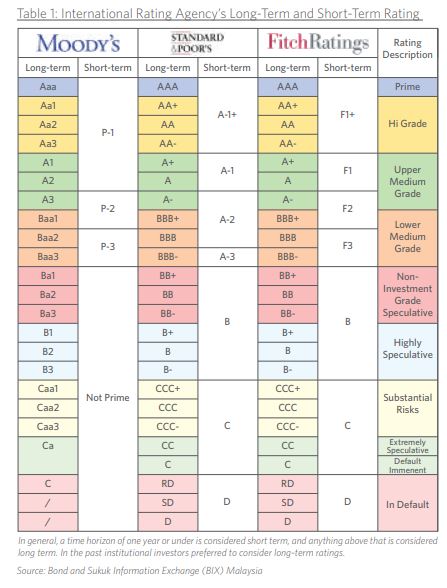

Investment Grade (IG) bonds

An Investment Grade rating indicates that a particular bond possesses a relatively lower risk of default. Hence, making it an attractive investment option for conservative investors. The yields are lower compared to high yield bonds.

High Yield (HY) bonds

Also known as ‘Junk’ bonds. These are higher paying interest rate instruments as they have a lower rating relative to Investment Grade bonds. A higher yield is to compensate investors for the additional risk taken. Certain high yield bonds are also called ‘fallen angels’ after losing their IG status.

Treasuries

Treasury securities (Treasuries) are deemed to be the safest investment instrument. It is also known as the risk-free rate. The guarantor behind these instruments is the full faith and credit of the US government.

Investors are guaranteed the return of both their interest and principal that they are due. Treasuries are also vulnerable to both inflation and changes in interest rates, just like any other bond instrument.

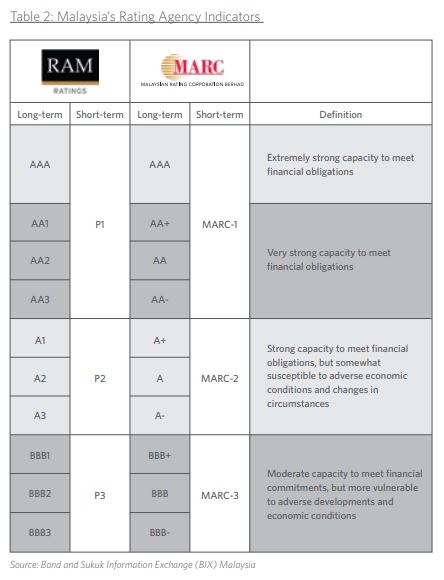

Malaysian Government Securities (MGS)

MGS are coupon-bearing, long-term bonds issued by Malaysia’s government to raise funds for development expenditures. It typically constitutes the most actively traded bonds in the country. Bank Negara Malaysia (BNM) regularly issues 3-year, 5-year, 7-year, and 10-year MGS as benchmark securities for the development of a benchmark yield curve. In addition, 15-year and 20-year have also been issued to lengthen the yield curve.(Source: Bond and Sukuk Information Exchange (BIX) Malaysia)

Government Investment Issue (GII)

GII is a long-term non-interest-bearing Government securities based on Islamic principles issued by the government of Malaysia for funding developmental expenditure. GII are issued through competitive auction by BNM on behalf of the government. GIIs are issued with original maturities of 3-year, 5-year, 7-year, and 10-year.(Source: Bond and Sukuk Information Exchange (BIX) Malaysia)

What is a Credit Spread?

The credit spread is the difference in yield between bonds that have a similar maturity, but different credit quality. It is an indication of the risk premium taken by a bond investor. It is typically measured against the US Treasury or a government bond as it is considered the risk-free rate.

For example, a AA-rated bond will have a narrower spread compared to a BB-rated bond because it is less risky due to a higher credit quality. Spreads are usually measured in basis points (bps), where 1 bps equals to 0.01%.

What does it mean when credit spreads widen or narrow?Credit spreads widening can be a signal of:-

• Potential distress in the bond issuer and its creditworthiness or;

• Markets turning more cautious due to the macro environment and investors becoming more risk-averse.

Hence, investors are being compensated with higher yields which is causing spreads to widen.

Credit spreads narrowing can be a signal of:-

• Potential improvements in the bond issuer and its creditworthiness or;

• Markets turning more ebullient because of improvements in the macro environment and sentiment

A healthy economic environment where demand for bonds remain strong will cause spreads to narrow or tighten.

Invest in Fixed Income

To learn more about our fixed income solutions and how you can build a diversified portfolio with bonds, book an appointment with us via the link here: aham.com.my/Book-An-Appointment